India’s Demographic Dividend: Are We Ready to Reap It?

Introduction

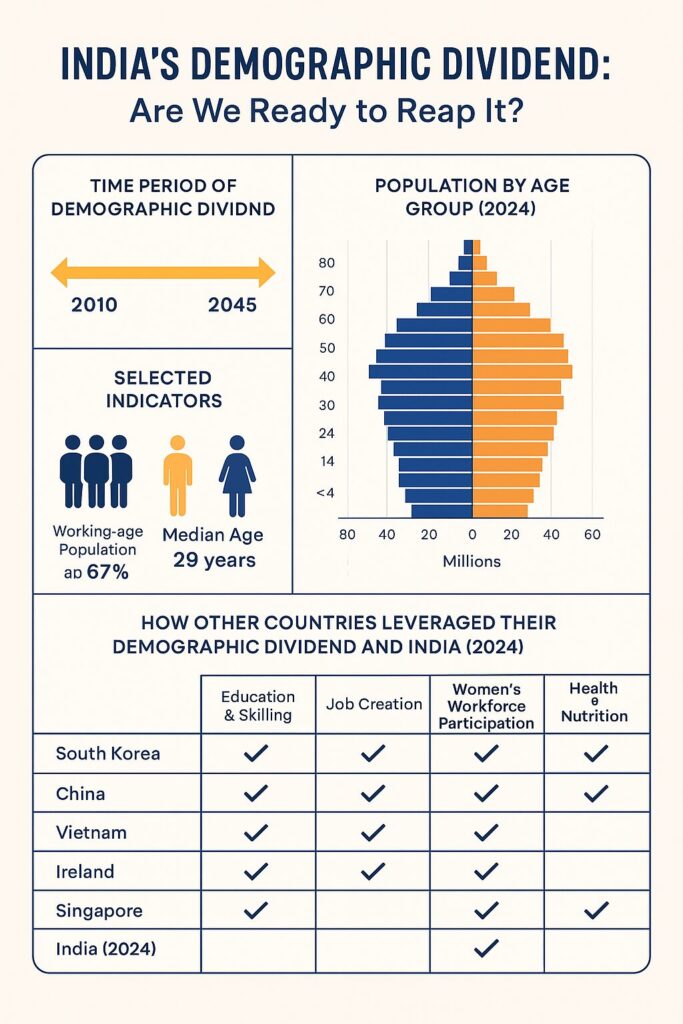

India stands at the crossroads of a historic opportunity—a phase known as the demographic dividend. With over 65% of its population below the age of 35 and a median age of just under 29 years (as of 2024), India possesses the largest youth population in the world. This window of opportunity, projected to last until around 2045, has the potential to transform India into a global economic powerhouse. However, the realization of this dividend is far from automatic. It depends on how well the country can educate, skill, employ, and integrate its youth into the economic mainstream.

This article examines the concept of India’s demographic dividend, lessons from other countries, and the current state of readiness across various sectors that influence demographic potential.

1. Understanding the Demographic Dividend

A demographic dividend refers to accelerated economic growth that results from changes in a country’s age structure, typically when the working-age population (15-64 years) becomes larger relative to the dependent population (children and elderly).

Phases of Demographic Transition

- High Birth and Death Rates: Pre-industrial era with low population growth.

- Declining Death Rates: Population grows rapidly.

- Declining Birth Rates: Working-age population increases relative to dependents.

- Aging Population: Working-age population shrinks, elderly rise.

India is currently in Phase 3, a window where its working-age population is growing and the elderly population remains relatively low.

2. India’s Demographic Profile

- Population: Approx. 1.43 billion (2024).

- Working-Age Population (15-64 years): About 67% of total.

- Median Age: ~29 years (vs. 38 in the U.S., 48 in Japan).

- Dependency Ratio: ~47%, steadily declining.

- Annual Labour Force Entrants: ~10–12 million.

The youth bulge is especially pronounced in states like Uttar Pradesh, Bihar, and Madhya Pradesh, while southern states like Kerala and Tamil Nadu are already entering the aging phase.

3. Global Experiences: How Others Reaped the Dividend

1. South Korea (1960s–1990s)

- Invested in universal education with a focus on STEM.

- Export-oriented manufacturing policies.

- Land reforms, health care access.

- Result: GDP per capita rose from ~$100 to ~$10,000.

2. China (1980s–2010s)

- One-Child Policy reduced dependency ratios.

- Created SEZs and became the “world’s factory.”

- Universal basic education and skills training.

- Result: Lifted 800+ million out of poverty.

3. Vietnam (1990s–present)

- Doi Moi reforms opened up markets.

- Focused on vocational skills and manufacturing.

- Maintained high literacy and basic healthcare.

- Result: 4x growth in GDP per capita.

4. Ireland (1990s–2008)

- Reformed education, encouraged FDI.

- Low corporate tax attracted tech giants.

- EU integration facilitated smart urbanization.

5. Singapore (1970s–1990s)

- Strategic urban planning and governance.

- Talent development and public housing.

- Became global financial and logistics hub.

Common Strategies:

- Invest in education, health, and infrastructure.

- Focus on manufacturing, export, and FDI.

- Promote female workforce participation.

- Ensure policy stability and governance.

4. Comparative Table: India vs Global Examples

| Parameter | South Korea | China | Vietnam | Ireland | Singapore | India (2024) |

| Education Reform | STEM focus | Universal | Basic, practical | Higher Ed overhaul | Early investment | Patchy outcomes |

| Skill Development | Industry-academia | Vocational scaled | Tied to manufacturing | Aligned with FDI | STEM-aligned | Fragmented schemes |

| Health | Universal access | Mass campaigns | Basic public health | Universal insurance | Strong public healthcare | High malnutrition, low spend |

| Labour Market | Reforms + protection | SEZs, job matching | Light manufacturing | Strong protections | Flexible market | Informal sector 85% |

| Female LFPR | 50%+ | ~60% | ~72% | ~55% | 60%+ | ~25% |

| Fertility Decline | 6 to 2 | One-child policy | Urbanization | Education-driven | Birth control | Regional disparity |

| Urban Infra | Transit, housing | SEZs, cities | Migrant absorption | EU funds | Best-in-class | Congested, unplanned in parts |

| Job Creation | Export-led | Manufacturing-led | Export-driven | Tech/finance | Strategic planning | Jobless growth |

| FDI Strategy | Partnered | Massive in SEZs | FTA-led | Low tax magnet | Efficient system | Moderate, improving |

| Governance | Developmental state | Central planning | Communist reforms | Stable democracy | High-efficiency | Democratic, but uneven execution |

5. Are We Creating Enough Jobs?

Employment Landscape

| Category | Value |

| Unemployment Rate (2024 est.) | ~7.5% (urban), ~4.2% (rural) |

| Youth Unemployment (15–24 years) | ~18–22% |

| Labour Force Participation Rate (LFPR) | ~40% (women’s LFPR ~25%) |

| Informal Employment | ~85% of total workforce |

Major Issues

- Jobless Growth: India’s GDP has been growing faster than job creation.

- Informalisation: High share of low-paid, low-security jobs.

- Underemployment: Many are working in jobs not matching their skills or education.

Sectoral Employment Breakdown

- Agriculture: 45% of workforce; low productivity.

- Manufacturing: 12–15%; stagnant job creation.

- Services: ~30%; mainly urban-oriented and skill-specific.

- Gig Economy: Growing but mostly precarious employment.

6. Education: Quantity vs. Quality

The Current Scenario

- Literacy Rate: ~77.7% overall; rural female literacy remains a concern.

- School Enrolment (Primary): >95%, but dropout increases after Class 8.

- Higher Education Gross Enrolment Ratio (GER): ~28%.

- Learning Outcomes: National Achievement Survey (2021) shows students 2-3 years behind expected levels.

Challenges

- Rote learning over critical thinking.

- Infrastructure gaps in rural and government schools.

- Poor linkage between curriculum and employment.

- Low faculty quality and research output in colleges.

Skill Mismatch

India ranks poorly in the Global Talent Competitiveness Index (Rank ~101 out of 134 in 2023), primarily due to lack of industry-aligned skills.

7. Skill Development: Are We Doing Enough?

Key Schemes

- Pradhan Mantri Kaushal Vikas Yojana (PMKVY): Aimed at skilling 10 million youth annually.

- Skill India Mission

- National Apprenticeship Promotion Scheme (NAPS)

Ground Realities

- Low Certification: Many trained youth lack nationally recognized certification.

- Employer Disconnect: Skills often don’t match job needs.

- Dropout Rates: High due to lack of incentives and awareness.

- Regional Imbalances: Southern and Western states see higher skilling success than BIMARU states.

Vocational Education

- Still stigmatized and lacks integration into mainstream schooling.

- Germany’s dual training model is a good example to emulate.

8. Women in the Workforce: An Untapped Resource

- Female Labour Force Participation: <25% compared to 60%+ in China and U.S.

- Barriers:

- Social norms.

- Safety concerns.

- Lack of formal jobs and flexible work options.

- Opportunities:

- Promote remote work.

- Support self-employment and SHGs.

- Improve access to childcare and sanitation.

Empowering women could raise India’s GDP by an estimated 18–20%, according to McKinsey.

9. Health and Nutrition: Foundation of Productivity

- Undernourishment: ~35% of children under 5 are stunted (NFHS-5).

- Anaemia: Over 50% of women aged 15–49 are anaemic.

- Mental Health: Rising issues among youth due to competition and digital overload.

- Public Health Spend: ~1.8% of GDP, lower than WHO recommended 3–5%.

Without a healthy and mentally fit workforce, demographic advantage becomes a burden.

10. Migration, Urbanisation, and Infrastructure

- India sees over 200 million internal migrants—mostly seasonal and informal.

- Rural to urban migration places stress on:

- Housing.

- Sanitation.

- Transportation.

- Healthcare.

- Smart Cities and AMRUT schemes aim to improve urban living conditions but coverage and implementation are patchy.

Proper urban planning is essential to absorb and integrate youth workforce effectively.

11. Digital Inclusion and Technology as Enablers

- Internet Penetration: Over 65% as of 2024.

- Digital India: Aimed at connecting remote areas with government and economic services.

- Startups and Innovation:

- India has over 110 unicorns.

- Youth are central to innovation and tech-driven entrepreneurship.

However, a digital divide remains:

- Rural vs urban access.

- Gender disparity in mobile/internet use.

- Need for digital skilling across socio-economic groups.

12. Policy Frameworks: Are They Sufficient?

Key Government Programs

- National Education Policy 2020: Focus on foundational literacy, critical thinking, and vocational training.

- Atmanirbhar Bharat: Aims to create self-sustaining industries and local job opportunities.

- Make in India: Manufacturing push.

- Startup India: Promoting entrepreneurship.

Implementation Gaps

- Fragmented schemes.

- Low monitoring and follow-up.

- Bureaucratic hurdles.

- Lack of convergence across ministries.

What’s needed is an inter-ministerial, long-term coordinated strategy focused solely on demographic dividend optimisation.

13. State-wise Readiness and Regional Imbalances

| Region | Readiness Index (Indicative) | Key Challenges |

| South & West India | High | Ageing faster; need to attract youth from other states |

| North & East India | Moderate to Low | Education and skill deficits; unemployment |

Bridging the Gap

- Encourage inter-state mobility.

- Improve governance and basic infrastructure in lagging states.

- Incentivise private sector investment in backward regions.

14. What If We Fail to Capitalise?

Failure to convert the demographic dividend into productive employment could lead to:

- Increased social unrest.

- Higher crime rates.

- Strain on welfare systems.

- Migration pressures on cities and abroad.

- A lost generation.

15. Recommendations: A Roadmap to Reap the Dividend

1. Education Reforms

- Improve quality and relevance of education.

- Integrate digital tools.

- Strengthen school-to-work transitions.

2. Massive Skill Development Push

- Align skilling with industry needs.

- Promote apprenticeships and practical training.

- Set up local skill hubs.

3. Create Jobs, Not Just Growth

- Labour-intensive sectors (textiles, tourism, construction) need incentives.

- MSME reforms and easier credit access.

- Strengthen public infrastructure to create employment.

4. Empower Women

- Targeted schemes for skilling, financing, and workplace safety.

- Legal reforms for flexibility in work hours, maternity benefits, etc.

5. Health and Nutrition Investment

- Increase public health spending.

- Special focus on adolescent and maternal nutrition.

6. Governance and Coordination

- One nodal ministry to monitor all demographic dividend-related programs.

- Data-driven decision-making.

- Partnerships with private sector, NGOs, and global institutions.

16. The Cost of Inaction

If India fails to leverage this opportunity:

- High unemployment and underemployment.

- Rising social unrest and crime.

- Brain drain and urban chaos.

- Increased welfare burden due to ageing population.

17. Roadmap: Reaping the Demographic Dividend

- Education: Improve quality, reduce dropout, emphasize digital and soft skills.

- Skills: Practical training, apprenticeships, industry linkages.

- Jobs: Labour-intensive sectors, ease of doing business, MSME support.

- Women: Flexible work, safety, incentives, skilling.

- Health: Nutrition, adolescent health, mental health inclusion.

- Governance: Nodal coordination, data-backed policymaking.

- Infrastructure: Urban planning, smart housing, mass transit.

18. Conclusion

India’s demographic dividend offers a once-in-a-generation opportunity. Countries like China, South Korea, and Vietnam showed that with strategic investments in human capital, governance, and infrastructure, such a phase can transform national fortunes.

India has the youth, the policies, and the potential. What it now needs is urgency, coherence, and consistent execution.

The next two decades will determine whether India becomes the next global economic leader or faces the grim prospect of a lost generation.

19. References

- UN Population Prospects 2022

- World Bank Country Reports

- NFHS-5

- McKinsey Global Institute

- ILO Global Employment Trends

- Economic Survey of India 2023–24

- Ministry of Skill Development Reports

- Global Talent Competitiveness Index 2023

- NITI Aayog State Reports