Circular Economy in India: Policy Gaps and Private Sector Opportunities

Introduction

A circular economy is an economic model focused on minimizing waste and making the most of resources. Unlike the traditional linear economy (take-make-dispose), a circular system aims to design out waste, keep materials in use, and regenerate natural systems. For a rapidly growing and resource-constrained country like India, adopting circular economy principles can significantly boost environmental sustainability, economic growth, and inclusive development.

As India advances toward becoming a $5 trillion economy, transitioning to a circular economy presents a multi-trillion-dollar opportunity, particularly in key sectors such as agriculture, electronics, automotive, construction, and textiles.

India’s Current Position on the Circular Economy

India has made several policy-level moves and sectoral commitments that touch upon circular economy principles. For instance:

- The National Resource Efficiency Policy (NREP) draft (2019) aimed to mainstream resource efficiency across sectors.

- Extended Producer Responsibility (EPR) under Plastic Waste Management Rules (2016, updated 2022).

- Swachh Bharat Mission, Smart Cities, and GOBARdhan Yojana (biogas from waste) support waste-to-wealth models.

However, a comprehensive and binding circular economy framework is still missing, and implementation remains uneven.

India’s Waste Statistics

- 62 million tonnes of municipal solid waste generated annually

- Only ~20% of this is processed or recycled

- $2 trillion potential gains from circular economy by 2050 (NITI Aayog)

Policy Gaps in India’s Circular Economy Journey

- Lack of Centralised Framework

No national law currently mandates circular principles across sectors. NREP remains in draft stage with no formal adoption. - Weak Enforcement of EPR

Compliance with EPR, especially in plastics and electronics, is weak. Many small producers operate outside regulatory frameworks. - Inconsistent Sectoral Coordination

Ministries such as MoEFCC, MoHUA, and MNRE run overlapping but fragmented programs. - Limited Incentives for Private Innovation

India lacks green public procurement standards, tax breaks, or funding guarantees for circular initiatives. - Poor Integration with MSMEs and Informal Sector

The circular model depends heavily on waste pickers, recyclers, and repair services, most of whom operate informally. - Data Deficiency

Little standardised data exists on material flows, reuse rates, and sectoral resource productivity.

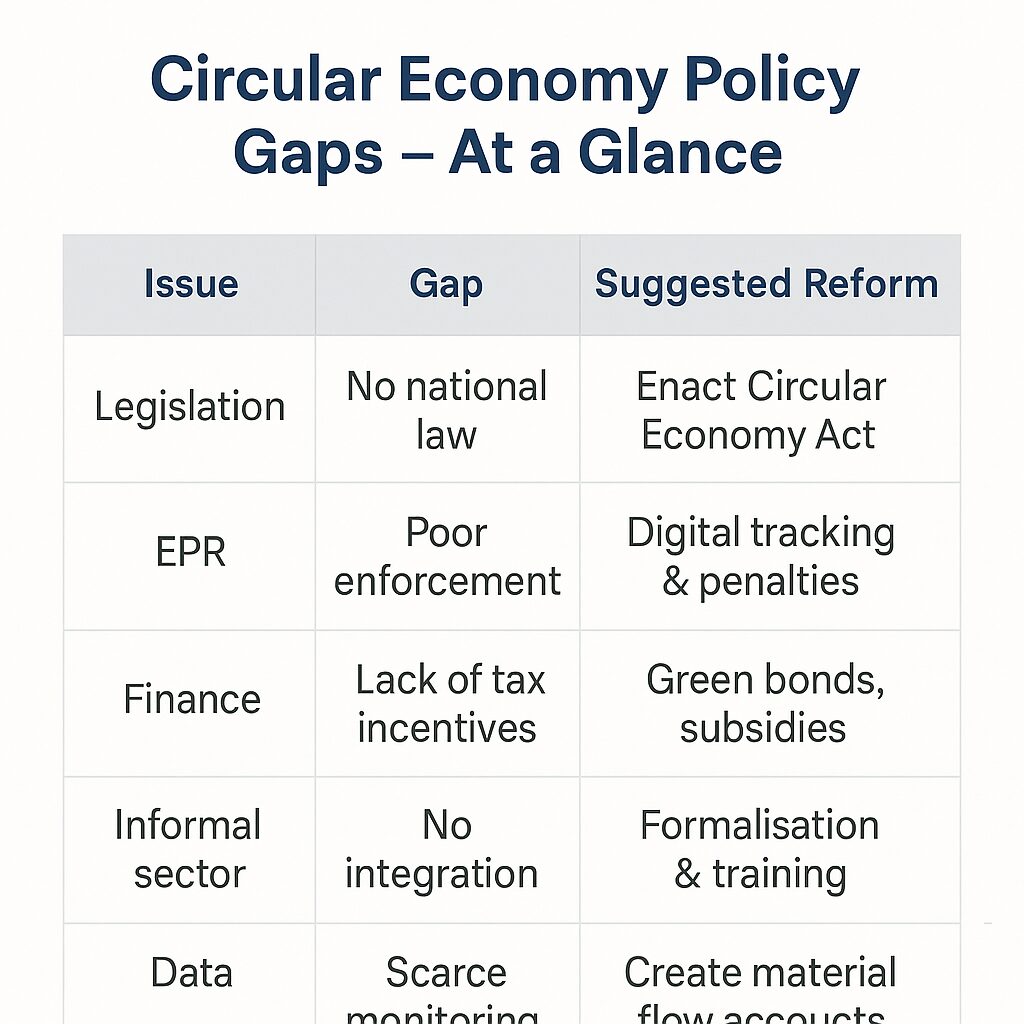

Circular Economy Policy Gaps

| Issue | Gap | Suggested Reform |

| Legislation | No national law | Enact Circular Economy Act |

| EPR | Poor enforcement | Digital tracking & penalties |

| Finance | Lack of tax incentives | Green bonds, subsidies |

| Informal sector | No integration | Formalisation & training |

| Data | Scarce monitoring | Create material flow accounts |

Private Sector Opportunities in India’s Circular Economy

- Recycling and Resource Recovery

- Urban Mining of e-waste, metals, and plastics offers major business potential.

- Startups like Attero Recycling and Recykal are scaling end-to-end recovery.

- Reverse Logistics & Sharing Platforms

- Growth in rental economy (Zoomcar, Rentomojo) and repair services (UrbanClap).

- Logistics for used goods collection is a major emerging sector.

- Green Construction & Demolition Waste Recycling

- C&D waste constitutes ~25% of urban solid waste.

- Companies like Ramky Enviro and Mahindra Waste to Energy are innovating.

- Bioenergy & Composting

- Agro-residues and food waste can be converted to biogas, compost, and bio-CNG.

- GOBARdhan and SATAT schemes encourage private investment.

- Packaging & Product Redesign

- FMCG majors (Unilever, Nestle) are investing in eco-friendly packaging.

- Startups offer biodegradable packaging from seaweed, bagasse, and mushroom waste.

- Digital Circular Platforms

- AI-driven supply chain optimization and material traceability tools are growing.

- Example: Chakra Innovation uses AI to recover carbon from diesel emissions.

Emerging Circular Economy Sectors in India

- E-waste: $1.5 billion market by 2025

- Biogas: 50,000+ potential units under SATAT

- C&D Waste: 150 million tonnes per year; less than 5% processed

- Green Packaging: CAGR of 12%

- Sharing Economy: Estimated $2 billion opportunity

Global Experiences: Lessons from Developed and Developing Economies

European Union

- The EU Circular Economy Action Plan (2020) includes clear targets for sustainable products, right to repair, and digital product passports.

- Countries like Netherlands aim for 100% circularity by 2050.

China

- China’s Circular Economy Promotion Law mandates resource use audits, product life extension, and industrial symbiosis.

- Large investment in eco-industrial parks, supported by tax incentives.

Japan

- Pioneered the “Sound Material-Cycle Society”, with advanced recycling systems and consumer participation.

- Over 20% of total industrial input now comes from recycled resources.

Brazil and South Africa

- Brazil incentivizes waste-to-energy and plastic recycling through producer cooperatives.

- South Africa supports circular startups via its Green Fund and skills training.

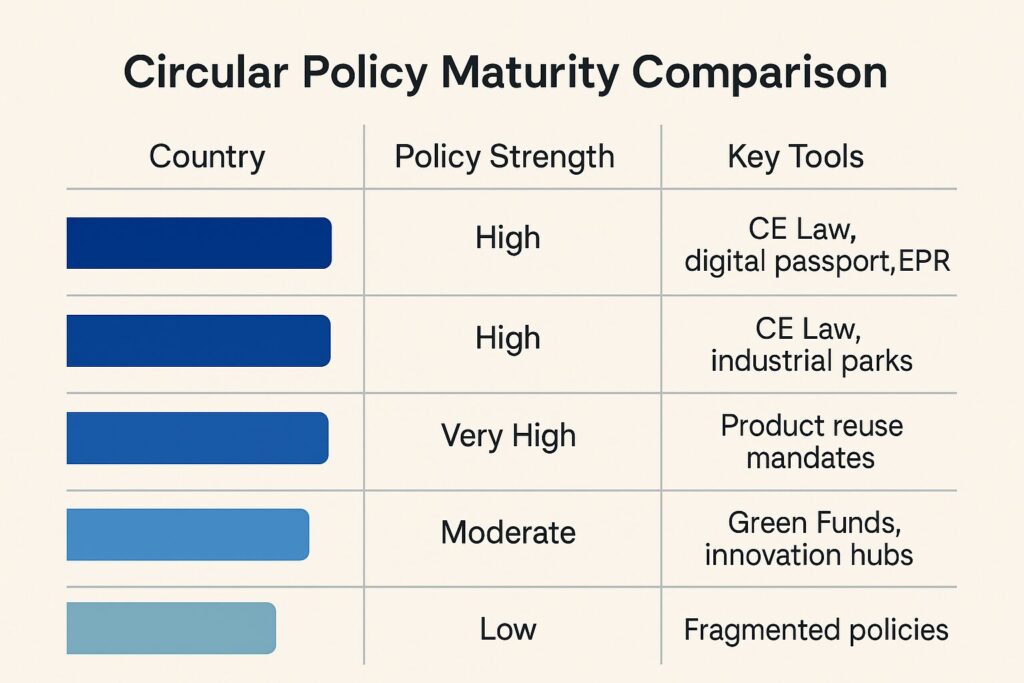

Circular Policy Maturity Comparison

| Country | Policy Strength | Key Tools |

| EU | High | CE Law, digital passport, EPR |

| China | High | CE Law, industrial parks |

| Japan | Very High | Product reuse mandates |

| South Africa | Moderate | Green Funds, innovation hubs |

| India | Low | Fragmented policies |

India’s Progress and Notable Success Stories

- E-waste Management: Attero Recycling is now exporting recycled metals globally.

- Plastic Circularity: Reliance Industries uses waste plastics for road construction.

- Circular Apparel: Brands like Doodlage, BLabel, and Bombay Hemp Co are redefining sustainable fashion.

- Urban Circularity: Indore and Pune have successful decentralized waste management systems involving local enterprises.

Investment Needs and Commercial Viability

- India needs ~$50–$80 billion in investments over 10 years for full-scale circular infrastructure (as per NITI Aayog).

- Private sector-led CE models in construction, mobility, packaging, and waste management can achieve break-even within 3–7 years, especially when supported by:

- Carbon credits

- CSR-backed initiatives

- Impact investment and blended finance

Investment & Job Potential of Circular Economy in India

- Total Investment Required: ~$80 Billion over 10 years

- Jobs Potential: 10–15 million by 2040

- Key Sectors: Waste, Repair, Bioenergy, Construction

- Circular Economy GDP Boost: 4.5% by 2050 (NITI Aayog projection)

Recommendations for Accelerating the Circular Economy in India

- Enact National Circular Economy Framework Law

- Strengthen and Digitize EPR Mechanisms

- Incentivize Circular Innovation with Fiscal Tools

- Formalise the Informal Sector

- Develop CE Clusters and Eco-Industrial Zones

- Foster Public-Private Partnerships (PPPs)

- Build Capacity Among MSMEs and Local Governments

- Promote Consumer Awareness through Labelling and Education

- Integrate Circular Economy into School & Vocational Curricula

Conclusion

India stands at a critical juncture where circular economy adoption is no longer optional but essential. With mounting environmental stress, growing population, and urbanisation, the only sustainable path forward lies in decoupling growth from resource consumption.

The private sector has a significant role to play—through technology, finance, design, and entrepreneurship—especially if the government enables the right ecosystem. Drawing from global experiences and leveraging India’s frugal innovation potential, a circular economy can power India’s green industrial revolution, generate jobs, and strengthen long-term resilience.

References

- NITI Aayog – Strategy for Resource Efficiency (2020)

- MoEFCC – Draft National Resource Efficiency Policy (2019)

- World Economic Forum (2023) – Circular Economy Opportunities in India

- Ellen MacArthur Foundation – Global CE Case Studies

- EU Circular Economy Action Plan (2020)

- CEEW – Mapping India’s Circular Economy Landscape

- Attero Recycling, Recykal – Industry Reports

- UNIDO Circular Economy Reports – India and Asia