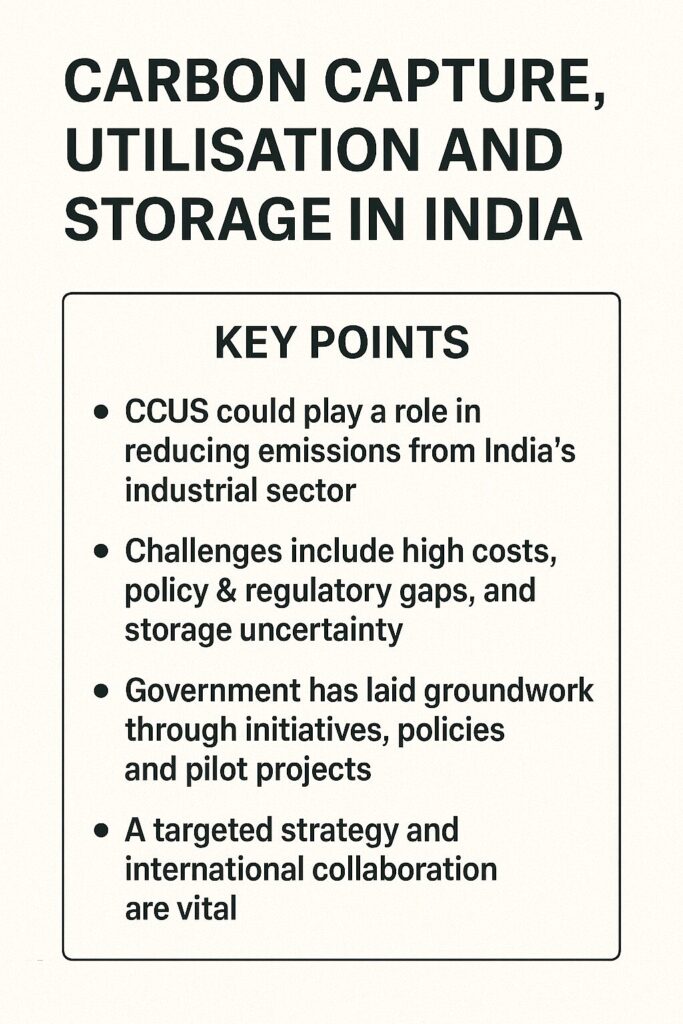

Carbon Capture, Utilisation and Storage (CCUS) in India: Reality or Mirage?

Executive summary (the “so what?”)

CCUS has moved from academic promise to early-market reality in India—but only for very specific use-cases. India now has: a handful of real projects (e.g., the Tuticorin “CO₂-to-soda-ash” plant), a flagship refinery-to-oil-field CO₂-EOR demonstration being engineered by IOCL and ONGC, newly approved CCU testbeds for cement, and a national programme under design with sizeable public funding. Globally, deployment is accelerating (Norway’s Northern Lights injected its first CO₂ in August 2025; the US and UK have created bankable policy models). Against that backdrop, India’s question isn’t whether CCUS works—it does—but where it is technically, geologically, and economically sensible, and how to get projects to final investment decision (FID). On balance, CCUS in India is a “targeted reality,” not a silver-bullet: compelling for cement, refineries, fertiliser, steel, blue hydrogen, and CO₂-EOR in specific clusters; far less attractive for old coal power retrofits without strong incentives and storage access. Reuters+5carbonclean.com+5spgindia.org+5

1) Why CCUS matters for India (and where it doesn’t)

- Hard-to-abate industries dominate India’s industrial emissions. Cement, steel, fertiliser, refining, and chemicals create process CO₂ streams that persist even with 100% renewable power. CCUS is one of the few options that can abate those streams at scale. India’s long-term low-carbon strategy explicitly flags future technologies like hydrogen and CCUS for hard-to-abate sectors. unfccc.int

- Energy security realities. Coal remains part of India’s power/industrial feedstock for years; policymakers are exploring CCUS alongside gasification and blue hydrogen to blunt emissions while capacity for non-fossil expands. In September 2025, officials outlined 50–100% public funding for select CCUS projects and confirmed coal capacity additions even as non-fossil targets rise. Reuters

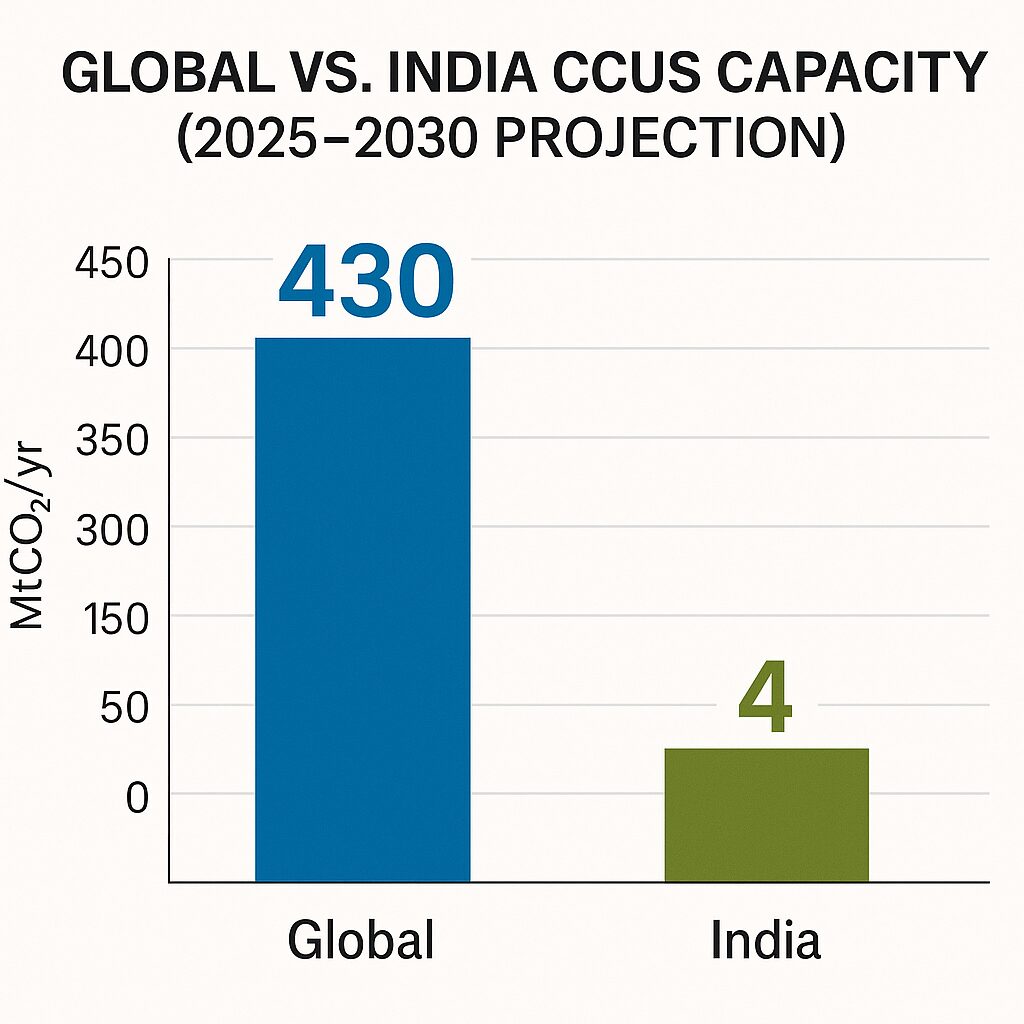

- Global momentum & learning curve. The IEA’s 2025 database shows ~50 Mt/yr capture operating worldwide and a 2030 pipeline ~430 Mt/yr. But only a fraction has reached FID—policy reliability makes or breaks viability. IEA+1

Bottom line: CCUS is not a licence to continue business-as-usual; it’s a surgical tool for emissions that are otherwise very expensive to eliminate.

2) India’s CCUS policy landscape (2022–2025)

- National framework. NITI Aayog released “CCUS Policy Framework and Deployment Mechanism” (Nov 2022), a blueprint identifying priority sectors, business models, and enabling policies. A 2025 NITI workshop focused on cement deployment barriers. Press Information Bureau+1

- Emerging public funding programme. Reports in Sept–Oct 2025 indicate a phased ₹38,900-crore CCUS scheme, with central support covering just over half the capex—complementing the 50–100% funding signals for pilot/priority projects. The Economic Times+1

- Sector testbeds. The Government approved five CCU testbeds in cement to de-risk capture at kilns, a critical test case for process emissions. The Times of India

- Carbon markets, a missing price signal. India notified the Carbon Credit Trading Scheme (CCTS) in June 2023; in Dec 2023 it added an Offset Mechanism with project registrations opening 1 Jan 2025. While not a carbon tax, the ICM/CCTS can underpin CCUS offtake via performance-based credits. Bee India+1

What’s still needed: storage regulations (MMV—monitoring, measurement, verification), pore-space and liability clarity, pipeline/port access rules, and long-term offtake contracts for CO₂ transport & storage (T&S). The NITI report and subsequent workshops point the way, but specific statutes and tariff models will decide bankability. Press Information Bureau+1

3) India’s project pipeline: from pilots to clusters

- Tuticorin (Tamil Nadu): Post-combustion capture + utilisation. At Tuticorin Alkali Chemicals, Carbon Clean’s solvent system captures CO₂ from a boiler flue gas and converts it into soda ash, with reported capture costs “around $30/t” at launch—an early global landmark. carbonclean.com+1

- IOCL Koyali → ONGC Gandhar (Gujarat): Refinery capture + EOR storage + blue H₂ linkage. A planned integrated project capturing CO₂ at IOCL’s Koyali refinery, piping ~80 km to ONGC’s Gandhar oilfield for CO₂-EOR, also enabling blue hydrogen. This is India’s first large integrated CCUS-cum-EOR design. spgindia.org+1

- Academic & storage pilots: IISER-Bhopal/CSIR-NGRI are drilling India’s first CO₂ injection well in Deccan basalts to validate mineralisation pathways—key for onshore storage. The Times of India

- Industrial testbeds: Five cement CCU testbeds (2025) will help crack capture-cost reduction and integration issues in kilns. The Times of India

- R&D infrastructure: Carbon Clean opened a large CCUS research hub in Navi Mumbai in 2025, signalling a domestic equipment/solvent innovation base. Offshore Energy

What’s missing: a coastal CO₂ shipping + offshore storage option (like Norway) and one or two multi-user onshore clusters with shared T&S that link refineries, cement plants, steel mills, and fertiliser units.

4) Geology & storage: does India have the “bank”?

Bankability hinges on safe, long-term storage:

- Depleted fields & saline aquifers. DGH’s draft 2030 CCUS roadmap synthesises storage capacity across seven oil-producing basins, indicating ~1.2 Gt viable (out of higher theoretical numbers), concentrated in basins like Cambay—suitable for EOR and saline storage with known subsurface. DGH India

- Basalt mineralisation (Deccan Traps). India hosts one of the world’s largest continental flood basalts (~500,000 km²). Studies estimate very large theoretical potential via rapid mineralisation, though heterogeneity and site-specific hydrogeology mean proven capacity needs pilots and MMV. The IISER-Bhopal injection-well effort directly targets this gap. nora.nerc.ac.uk+2ResearchGate+2

- Cambay basin specifics. Recent work places Cambay storage estimates (depleted fields) in the hundreds of Mtrange; practical capacity will depend on pressure management, plume migration, and caprock integrity. ScienceDirect

Implication: India likely has adequate storage for an initial multi-decadal CCUS programme—but definitive capacity requires step-wise appraisal (seismic, test injections, MMV baselines) and a storage-licensing regime.

5) Where the economics close—and where they don’t

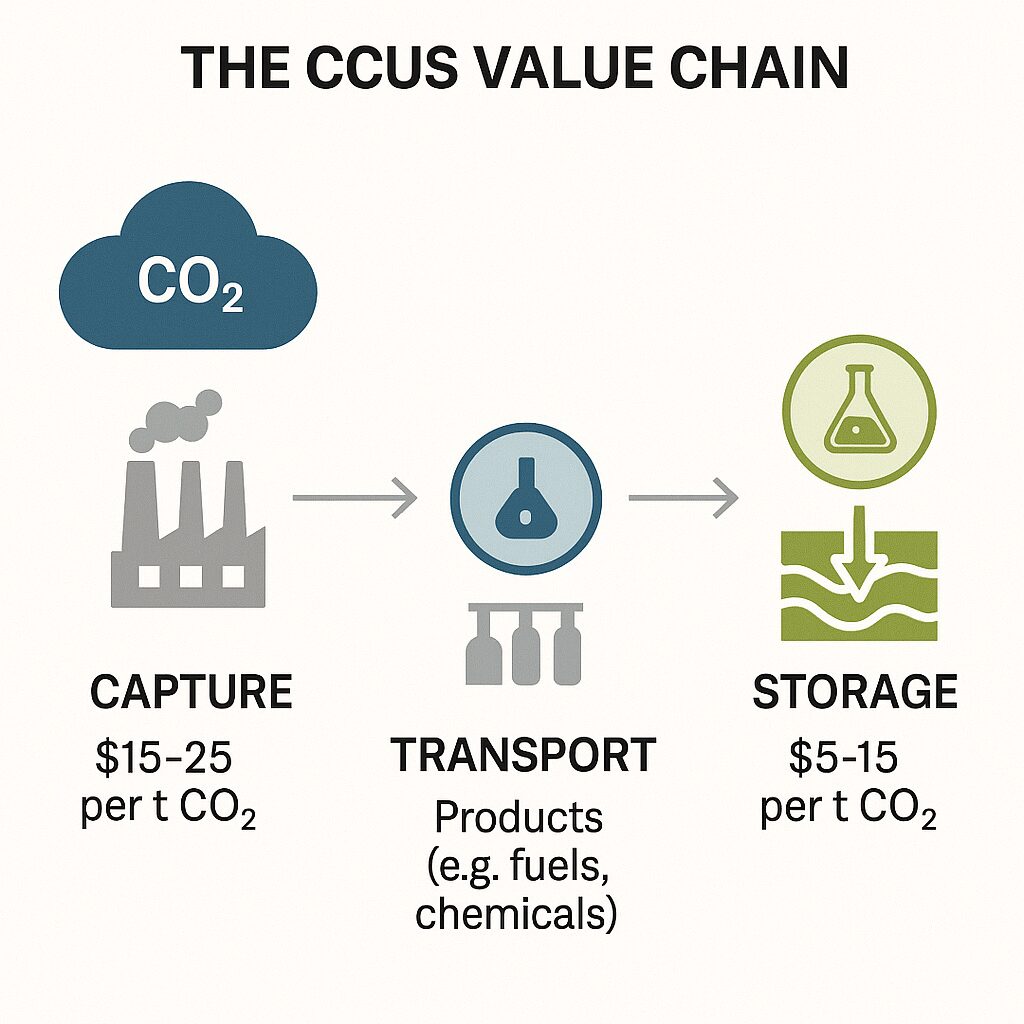

Capture costs vary by source purity and scale:

- Low-hanging fruit: high-purity streams (ammonia/urea, hydrogen/SMR, ethylene oxide) can hit $30–60/tCO₂capture; cement and refineries tend to be $70–120/t today, trending down with scale/learning; coal power retrofits often exceed $100–150/t unless integrated with EOR or subsidised transport/storage. The Tuticorin project demonstrated a ~$30/t benchmark for a specific utilisation pathway. carbonclean.com

Revenue/incentive stack determines viability:

- India’s evolving stack: central capex support (₹38,900-crore programme), 50–100% funding for select projects, and the CCTS/ICM to create monetisable credits. Together they can close part of the gap, especially for cement/refineries. The Economic Times+2Reuters+2

- Global reference models to emulate:

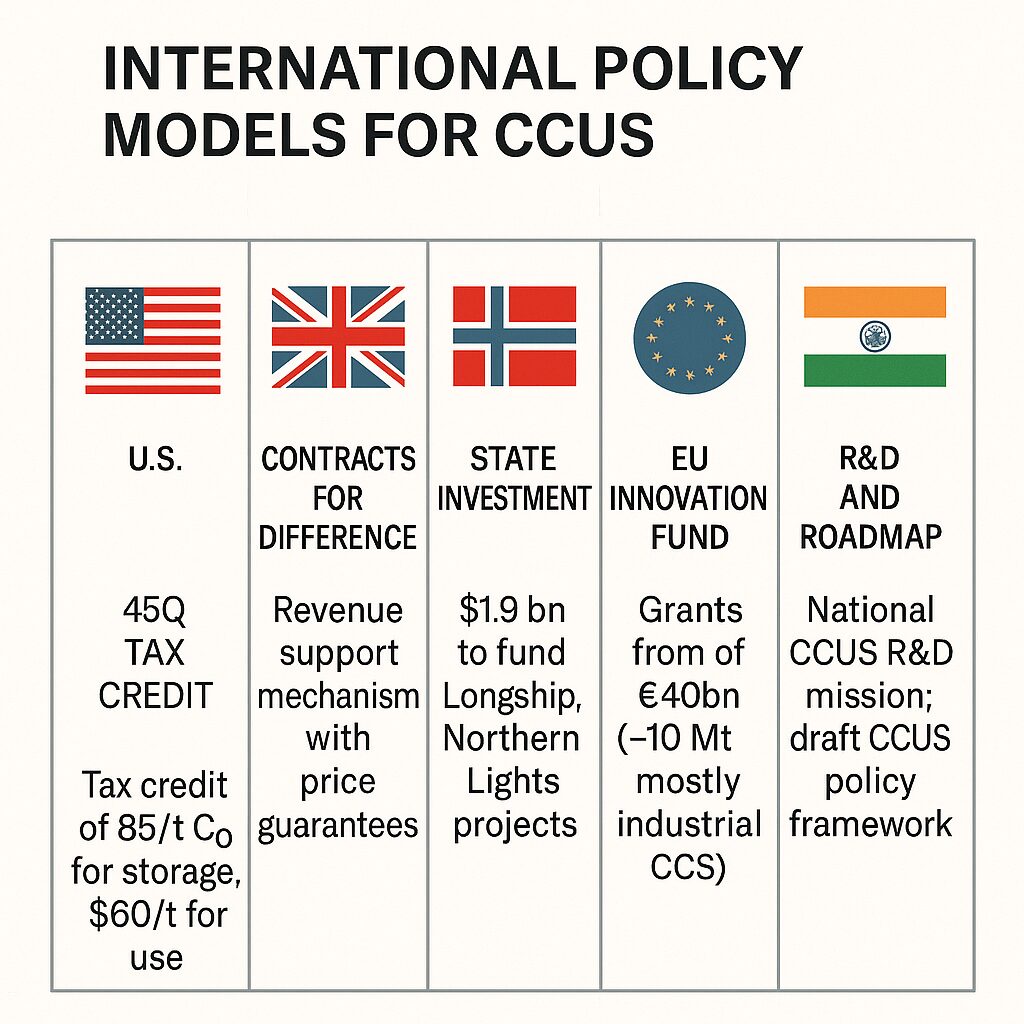

- United States—45Q: $85/t (saline storage) and $60/t (EOR) for 12 years (higher for DAC), which has unlocked a wave of projects. U.S. Energy Information Administration+1

- United Kingdom—cluster model: government-backed T&S networks (HyNet, East Coast) with regulated returns and long-term contracts; Track-1 approved in 2024/2025. GOV.UK+1

- European Union—Innovation Fund: multi-billion-euro grants from ETS revenues to de-risk first-of-a-kind CCUS in industry. Bellona EU+1

- Norway—Longship/Northern Lights: state-supported CO₂ shipping & offshore storage hub now operational (Aug 25, 2025) with 1.5 Mt/yr in Phase-1, expanding to >5 Mt/yr. Reuters+1

Indian takeaway: Marry capital grants with operational credits (via CCTS), long-term T&S contracts, and cluster infrastructure to compress unit costs and reach FID.

6) Priority Indian use-cases (2025–2035)

- Cement (process CO₂):

- Why CCUS: ~60–65% of emissions are from calcination (not energy), making electrification/RE less effective.

- What to do: Deploy capture at large integrated plants; create limestone-belt hubs with shared CO₂ compression, pipelines, and either onshore saline/basalt storage or coastal shipping. The five national testbeds can standardise integration and solvent choices. The Times of India

- Refineries & petrochemicals (hydrogen/SMR streams):

- Why CCUS: High-purity H₂/CO₂ streams are cheap to capture; blue hydrogen integrates naturally.

- What to do: Replicate the Koyali→Gandhar template in Jamnagar, Hazira, Paradeep, and coastal corridors; link to EOR where available and to saline/basalt storage where not. spgindia.org

- Fertiliser (ammonia/urea CO₂):

- Why: High-purity CO₂; some plants already vent concentrated CO₂.

- What to do: Convert “vented CO₂” to storage or long-lived products (e.g., mineralisation), using short laterals to hub trunks.

- Steel (BF-BOF and DRI):

- Why: Near-term, capture from BF gas/DRI reformers; long-term, shift to green H₂-DRI.

- What to do: Pilot capture at large BF-BOF sites and link to clusters; co-deploy waste-heat use to reduce energy penalty.

- Coal power (selective):

- Why: Misfit for most legacy units; better for new supercritical units sited inside clusters with cheap T&S and strong incentives, or when tied to EOR.

- What to do: Limit to anchor units in hubs; otherwise prioritise renewables + grid flexibility.

- Blue hydrogen & gasification:

- Why: India is assessing coal-to-SNG and refinery hydrogen decarbonisation; capture is integral to the proposition.

- What to do: Align with national hydrogen strategy; reserve storage volumes early. Reuters

7) Build it like a utility: hubs, pipes, ships, and stores

The cluster approach reduces costs by sharing infrastructure:

- Onshore clusters: Jamnagar-Hazira-Dahej (Gujarat), Mumbai-Raigad-Navi Mumbai (Maharashtra), Paradeep-Dhamra (Odisha), Vizag-Kakinada (Andhra), and the limestone belt across central/north India for cement.

- Offshore option: Develop CO₂ shipping terminals and leased offshore storage (Norway-style) while domestic storage is appraised—this narrows “first-mover” risk. Reuters

- Contracts & regulation: Treat T&S as a regulated utility with predictable tariffs and open access (UK model). GOV.UK

8) Risks and safeguards

- Storage integrity & liability: Establish a licensing code for site characterisation, injection permits, MMV plans, and post-closure transfer of liability to the state after a defined monitoring period.

- Water/energy penalty: Capture adds parasitic load and solvent management; testbeds should quantify water balances and local impacts. NITI Aayog

- Utilisation quality: Prioritise long-lived CO₂ uses (mineral carbonation, building materials) over short-lived beverages to ensure genuine abatement.

- “Lock-in” risk: Use CCUS as a bridge for essential industries, not an excuse to prolong inefficient assets.

9) What leading countries did right—and what India can adapt

- United States (45Q): Simple, scale-dependent production tax credit per tonne stored; bankable for lenders; complements state grants. Lesson: A clear, long-tenor per-tonne incentive derisks offtake. U.S. Energy Information Administration

- United Kingdom (cluster contracts): Government underwrites T&S networks and offers revenue support to capture plants; phased Track-1/Track-2 competitions created demand visibility. Lesson: Build shared pipes & stores first, then connect emitters. GOV.UK

- Norway (Longship/Northern Lights): State co-funding created open-access storage; first CO₂ injections in 2025, with shipping logistics proven from third-party emitters. Lesson: Start with a national anchor and open access to crowd-in industry. Reuters

- European Union (Innovation Fund): Big, competitive capex grants from ETS revenues for first-of-a-kind industrial CCUS. Lesson: Pair grants with a rising carbon price to sustain projects beyond commissioning. Bellona EU

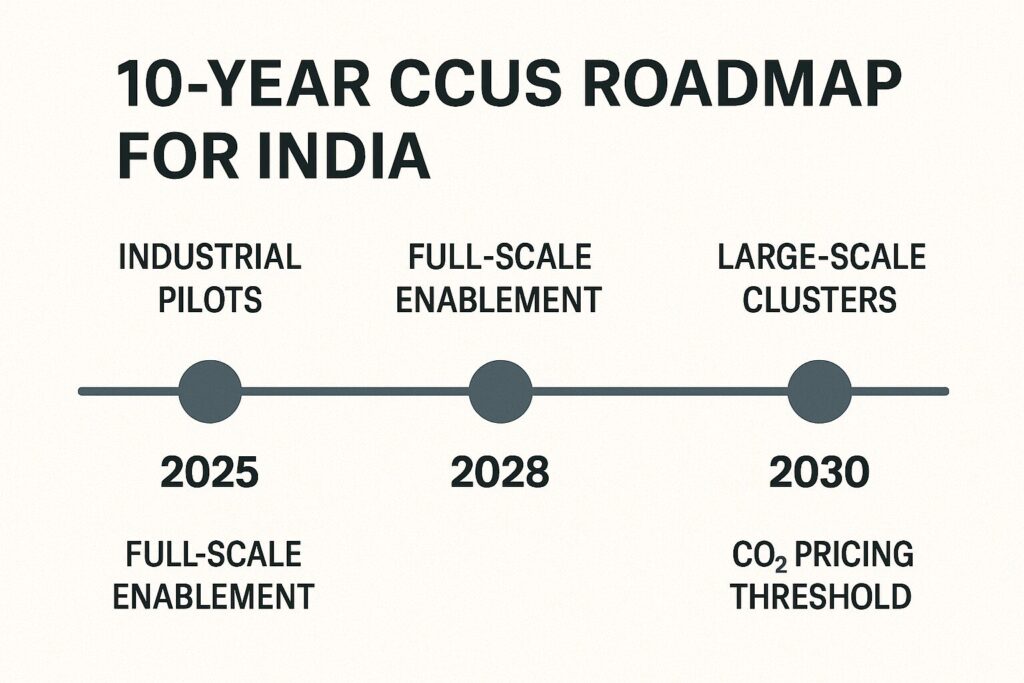

10) A pragmatic 10-year India playbook (2025–2035)

- Legislate the “missing middle”:

- Storage licensing & long-term liability transfer; CO₂ quality specs; third-party access; MRV/registry rules integrated with CCTS so that stored tonnes generate credits without double-counting. Bee India

- Fund two anchor clusters to FID:

- West coast (Gujarat/Maharashtra) and east coast (Odisha/AP) with CO₂ pipelines + coastal shipping; enable offshore storage access via international arrangements while domestic sites mature. Reuters

- Back “fast-wins” projects:

- Refinery hydrogen (blue H₂), fertiliser, and cement testbeds → full-scale capture at 2–3 kilns per cluster; replicate Koyali→Gandhar where subsurface is favourable. spgindia.org+1

- Make the money stack add up:

- Blend capital grants (≥40–60%) with performance credits under CCTS; allow contracts-for-differenceon capture OPEX against a reference carbon price.

- Storage appraisal sprint (basalt + basins):

- Fund seismic, wells, and pilots in Cambay, KG, and Deccan basalts (mineralisation). Publish a CO₂ Storage Atlas–India with bankable capacities and screening rules. DGH India+1

- Stand up a national T&S company (public-private):

- Think GAIL-like for CO₂ networks; regulate returns; ring-fence long-term stewardship funds from a per-tonne T&S fee.

- Guarantee of origin for stored CO₂ & product standards:

- Enable “low-carbon cement/steel” labels to monetise abatement premiums in domestic procurement and exports.

11) Is CCUS in India a reality or a mirage?

Reality, if we stay disciplined about five truths:

- It’s not for everything. CCUS is surgical—best for cement, blue H₂, refineries, fertiliser, and some steel pathways. Coal power retrofits are the exception, not the rule.

- Storage is king. Prove and permit safe, monitorable storage (basins + basalts). The IISER-Bhopal basalt injection and Gandhar EOR designs are right moves. The Times of India+1

- Clusters or bust. Shared pipes, ports, and stores cut costs and de-risk bankability—learn from UK clusters and Norway’s open-access store. GOV.UK+1

- Pay per tonne. A simple, durable ₹/t stored credit (CCTS-linked) plus capex grants is what unlocked scale elsewhere (US 45Q, EU IF). U.S. Energy Information Administration+1

- Transparency builds trust. MRV, public dashboards of injected/stored CO₂, and robust groundwater/induced-seismicity safeguards are non-negotiable.

If India executes on these, CCUS becomes a real decarbonisation lever that preserves industrial competitiveness and export access in a carbon-constrained world. If not, it risks becoming a mirage—expensive pilots without the pipelines, pores, and policies to scale.

12) Short case notes

- Tuticorin (Tamil Nadu): 200 TPD capture for soda ash production using Carbon Clean’s technology; a rare “utilisation that truly displaces fossil feedstock” case. carbonclean.com

- Koyali→Gandhar (Gujarat): Integrated capture + pipeline + EOR + blue H₂ concept by IOCL & ONGC; the right kind of complex, multi-asset demonstration India needs. spgindia.org

- Cement CCU Testbeds (2025): Government-approved five sites to prove kiln-integrated capture at scale. The Times of India

- Basalt mineralisation pilot: IISER-Bhopal/CSIR-NGRI well to validate rapid carbonate formation in Deccan Traps—critical for onshore options. The Times of India

13) Frequently asked questions (for boards & policymakers)

Q1. Will CCUS “lock-in” fossil fuels?

Not if targeted at unavoidable process emissions and paired with a renewables-heavy grid plan. It should acceleratenet-zero in heavy industry, not prolong inefficient assets.

Q2. Is offshore storage essential?

Not essential, but hugely helpful for first movers. Norway shows that CO₂ shipping + open storage can de-risk early projects while India appraises domestic sites. Reuters

Q3. How do we keep costs down?

Cluster build-out, long-lived utilisation (e.g., mineralised products), learning-curve effects (solvents, heat integration), and stable ₹/t incentives.

Q4. Can CCUS make Indian exports compliant with CBAM-type regimes?

Yes—if MRV is robust and product standards (low-carbon cement/steel) align with buyers’ rules.

14) A practical checklist for an Indian CCUS investment memo

- Source fit: high-purity CO₂? steady load factor?

- Cluster location: <100 km to hub? pipe ROW? port access?

- Storage access: signed T&S term sheet? delineated capacity? MMV plan?

- Policy stack: grant eligibility + CCTS credit pathway + state incentives. Bee India

- Unit economics: levelized capture cost (₹/t) + T&S tariff + credits; sensitivity to power and solvent costs.

- Offtake & certification: product low-carbon claim, third-party verification, export compliance.

Glossary (quick reference)

- CCUS: Carbon Capture, Utilisation and Storage—capturing CO₂ from point sources or air, using it in products or storing it underground.

- CO₂-EOR: Enhanced Oil Recovery using injected CO₂ to increase reservoir pressure and sweep oil; can store CO₂ if managed for net storage.

- Blue Hydrogen: Hydrogen from natural gas or other fossil feedstocks with CCUS applied to reformer/shift CO₂ streams.

- Saline Aquifer: Deep, salty water-bearing rock layer suitable for permanent CO₂ storage.

- Basalt Mineralisation: Chemical reaction of CO₂ with basaltic rocks to form stable carbonates (e.g., magnesite), enabling rapid, secure storage.

- Cluster/Hub: A shared network linking multiple emitters to common CO₂ transport and storage infrastructure.

- MMV (or MRV): Monitoring/Measurement & Verification—protocols to prove CO₂ is captured, transported, and stored safely and permanently.

- CCTS/ICM: India’s Carbon Credit Trading Scheme / Indian Carbon Market—framework to issue, trade, and retire emission credits from compliance and offset projects. Bee India

References (selected)

- NITI Aayog. CCUS Policy Framework & Deployment Mechanism (Nov 29, 2022); NITI cement workshop report (Jan 16, 2025). Press Information Bureau+1

- Government moves on funding & pilots: ₹38,900-crore phased CCUS programme; five cement testbeds approved. The Economic Times+1

- India’s national carbon market: CCTS notification (June 30, 2023); Offset Mechanism (Dec 2023) with registrations from Jan 1, 2025. Bee India+1

- Flagship Indian projects: Tuticorin CO₂→soda ash plant (Carbon Clean); IOCL Koyali → ONGC Gandhar CO₂-EOR design. carbonclean.com+1

- Storage geology: DGH Draft 2030 Roadmap (basin capacities); Deccan basalts mineralisation potential; IISER-Bhopal injection well. DGH India+2nora.nerc.ac.uk+2

- Global comparators: IEA CCUS database update (2025); Norway Northern Lights first injections (Aug 25, 2025); US 45Q; UK Track-1; EU Innovation Fund. Bellona EU+4IEA+4Reuters+4

Final verdict

CCUS in India is neither panacea nor placebo. Done right—in clusters, with proven storage, and a simple, durable ₹/t support—it is a targeted reality that can decarbonise the industrial spine of the economy while renewables, electrification, and green hydrogen scale. Done wrong—without storage proof, incentives, or shared infrastructure—it becomes a mirage that burns capital without cutting carbon. The choice is ours; the blueprint now exists, and the first-wave projects are on the runway.

—————————————————————————————————

Masterji, a very insightful analysis.

Thanks for your observation.