India Is Ageing: Why Pensions Matter Now More Than Ever

India is entering a decisive phase of its demographic and economic transition. For decades, the country benefited from a youthful age structure: a large working-age population supported relatively fewer elderly citizens. That advantage is now weakening. Life expectancy is rising, fertility is falling, family structures are changing, and migration is reshaping household support. The question India must answer is simple but enormous: how will the country ensure a dignified old age for hundreds of millions of citizens without placing unsustainable pressure on public finances and on the next generation of workers?

This is not a “future” problem. It is a governance problem that begins now—because pension outcomes are shaped over decades. If pension coverage and contribution discipline are not built during working years, no policy announcement at retirement can compensate fully.

1) India is ageing—faster than many assume

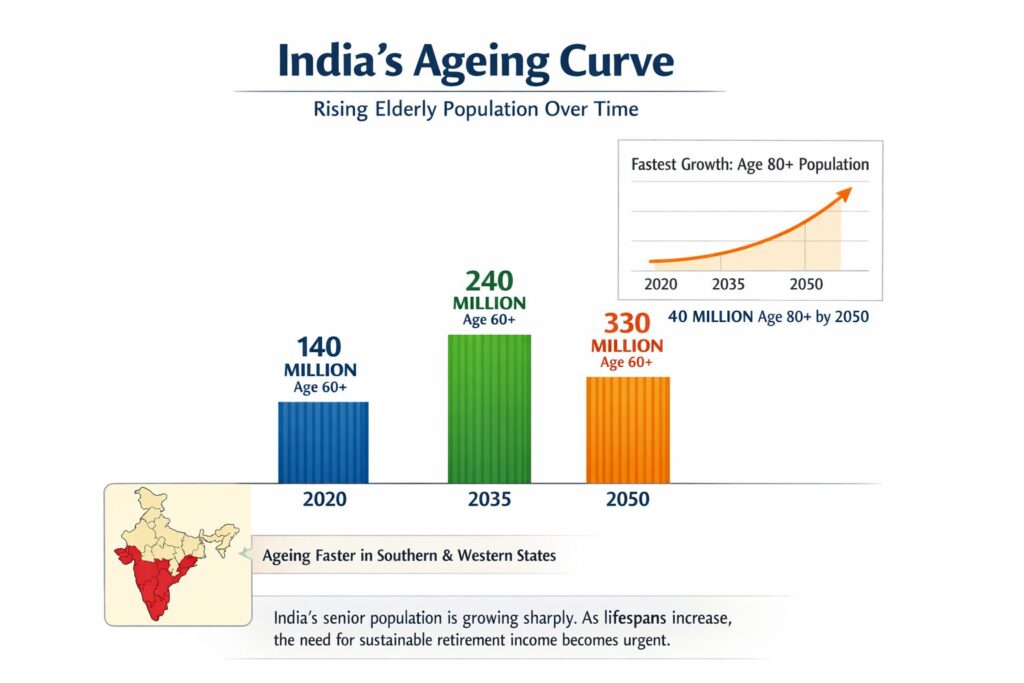

Ageing is not just “more seniors.” It changes the economic dependency ratio—fewer workers per retiree. It also changes the composition of old age: the 80+ group grows rapidly, with higher healthcare needs and dependency. This matters because living longer is a success story, but it transforms pension math: retiring at 60 and living to 80–85 means retirement income must last 20–25 years, often with rising medical expenses in the later years.

Ageing is also uneven across India. Some states, particularly in the south and parts of the west, are ageing earlier. This means pension and healthcare pressure will not arrive uniformly; some state budgets will feel it sooner.

India’s ageing will reshape retirement security. Over the next two decades, the 60+ population rises sharply, and the 80+ group grows even faster—exactly when healthcare costs and dependency risks increase. A pension system designed mainly for short retirements and stable payroll jobs will struggle. The question is not whether India will age, but whether it will build income security early enough to prevent distress later.

2) The family safety net is weakening (even if families remain supportive)

India has historically relied on family-based old-age support—joint families, co-residence, and intergenerational transfers. That support is still culturally strong, but it is becoming less reliable as a system. Urbanisation, migration for work, nuclear families, women’s workforce participation, and higher living costs reduce the capacity for consistent elder support.

This is especially important for the “oldest-old.” As people live longer, more elders will face advanced-age dependence. Widowed women are disproportionately represented in this cohort, and they often have lower lifetime savings and weaker property or income security.

India’s ageing will reshape retirement security. Over the next two decades, the 60+ population rises sharply, and the 80+ group grows even faster—exactly when healthcare costs and dependency risks increase. A pension system designed mainly for short retirements and stable payroll jobs will struggle. The question is not whether India will age, but whether it will build income security early enough to prevent distress later.

3) Informality is the central pension design challenge

A pension system works best when most workers contribute regularly over long periods. India’s labour market is still dominated by informal or semi-formal work where incomes fluctuate and employer-linked benefits are limited. Pension design therefore must work for:

- self-employed workers and micro-entrepreneurs

- gig/platform workers with variable earnings

- migrant and seasonal workers

- women with career breaks and unpaid care roles

- small enterprises that struggle with compliance complexity

If the system assumes stable monthly payroll contributions, it will leave large parts of India outside meaningful coverage.

4) The debate must move from enrolment to outcomes

India has built many pension schemes and platforms. Some have grown dramatically in subscriber count. But the real test is not how many accounts exist. The test is: Will retirees receive a predictable monthly income that lasts for life—especially beyond age 75 when medical and dependency costs rise?

This shift—from celebrating enrolment to measuring retirement outcomes—is the most important change India needs in how it thinks about pensions.

Bridge to Article 2:

To fix a system, we must first understand it clearly. India doesn’t have one pension system; it has multiple pillars that overlap unevenly. In Article 2, we’ll map India’s pension architecture in plain language—and show why outcomes differ sharply by occupation and income.

REFERENCES — ARTICLE 1

India Is Ageing: Why Pensions Matter Now More Than Ever

Demographics, Ageing & Dependency

- UNFPA India

India Ageing Report 2023: Unlocking the Potential of Older Persons in India

– Primary source for ageing trends, growth of 60+ and 80+ population, gender and regional dimensions. - United Nations – Department of Economic and Social Affairs (UN DESA)

World Population Prospects (Latest Edition)

– Authoritative global population projections, life expectancy, and dependency ratios. - Economic Advisory Council to the Prime Minister (EAC-PM)

Quality of Life in India Report (2023)

– Old-age dependency ratios, demographic transition, and long-term implications for India. - World Bank

Population Ages 65 and Above (% of Total Population)

– Cross-country comparison of ageing trajectories.

Family Structure & Social Change

- UNFPA & UN Women

Gendered Dimensions of Ageing

– Feminisation of ageing, widowhood, care burden, and income vulnerability. - National Sample Survey Office (NSSO)

Household Social Consumption & Migration Surveys

– Evidence on migration, nuclearisation of families, and elder living arrangements.