India’s Pension System Today: Who Gets What and Why Many Pensions Stay Small

Most Indians hear acronyms—EPF, EPS, NPS, APY—and feel the system is too complex to understand. The simplest way to make sense of India’s pension landscape is to stop thinking of it as a single scheme. India has multiple pillars, created at different times for different worker groups. The outcome is a system that can work well for some citizens, but remains thin or unreliable for many others.

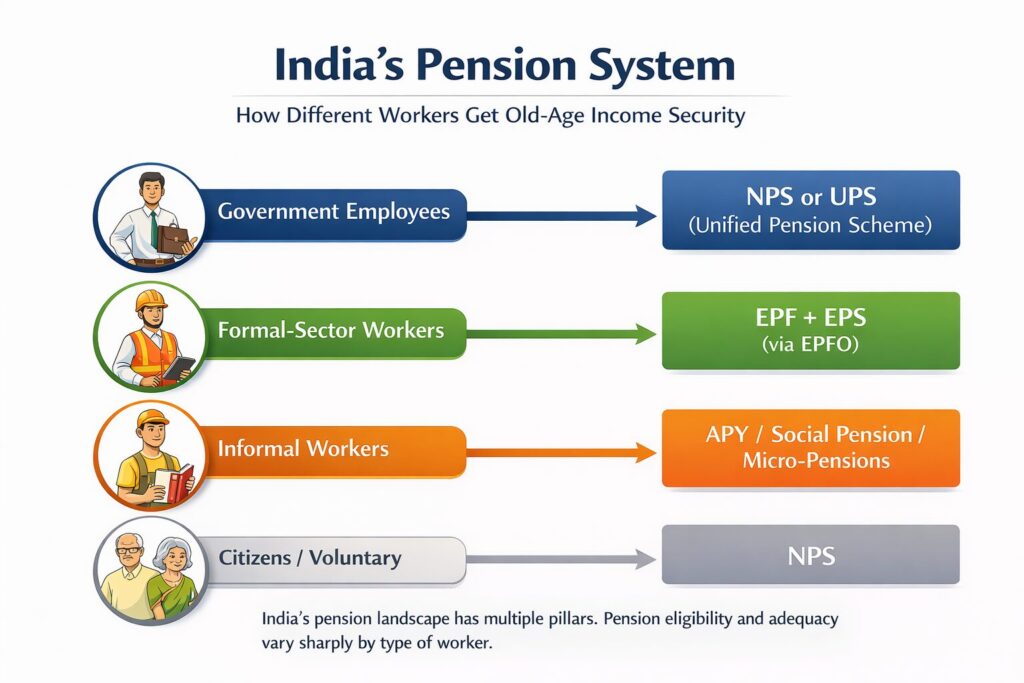

1) The four pillars of India’s pension ecosystem (plain-language map)

Pillar 1: Tax-funded pensions and social assistance

This includes legacy defined benefit arrangements (where they exist for certain employee cohorts) and targeted social pensions for vulnerable elderly citizens. These benefits are important for poverty prevention but vary in adequacy and coverage across states and schemes.

Pillar 2: Mandatory contributory schemes for formal workers (EPFO)

- EPF is primarily a retirement savings pool, commonly accessed as a lump sum.

- EPS is the monthly pension layer, but benefits can be modest for many retirees, raising recurring adequacy concerns.

Pillar 3: Regulated defined-contribution retirement platform (NPS)

NPS is a market-linked, portable retirement savings system regulated under a national framework. It has enabled large-scale retirement accounts across employment types, and has been expanded beyond government employees to citizens and corporate employees as well.

Pillar 4: Micro/guaranteed pension pathways for informal workers (APY and similar schemes)

APY has achieved very large enrolment. It is a major success in onboarding informal workers into a pension-like framework. The deeper issue is that many subscribers choose the lowest benefit slab, making retirement income too small to be protective.

.

India’s pension system is best understood as overlapping pillars built for different worker groups. The same retirement age can produce very different outcomes depending on whether one is a government employee, a formal-sector worker, or an informal worker. This map explains why India can simultaneously have large pension enrolment and yet face widespread old-age income insecurity—because contribution continuity and benefit adequacy vary sharply across pillars.

2) The key truth: India’s pension outcomes depend heavily on where you work

A government employee’s pension pathway, a formal-sector worker’s pathway, and an informal worker’s pathway can look completely different. This creates an outcome gap where some retirees enjoy predictable income, while many others reach old age with either no pension or pension-like savings that do not translate into adequate monthly income.

3) The system’s core problems: coverage, adequacy, and “income-for-life” design

Coverage gaps:

Even where accounts exist, regular contributions are not guaranteed—especially for informal and intermittent workers, women with care responsibilities, migrants, and those in very small firms.

Adequacy gaps:

A pension that cannot buy essentials—especially healthcare—does not provide dignity. Low monthly payouts undermine trust and push people back to dependence on family support or ad-hoc government relief.

Decumulation gaps (the most under-discussed issue):

Saving is not the end of pension design. The crucial question is: how does a retiree convert a corpus into stable lifelong income?

If retirement products encourage large lump-sum withdrawals without strong lifelong-income defaults, many people will exhaust savings in their later years—precisely when medical and dependency expenses rise.

4) The “coverage vs adequacy” gap explains why enrolment numbers can mislead

India’s platforms can show large subscriber numbers, but outcomes depend on:

- contribution levels

- contribution regularity

- investment horizon

- and the rules/defaults at retirement (annuity vs lump sum vs systematic withdrawals)

The pension debate must therefore shift from “How many are enrolled?” to “How many will retire with income security for 20–25 years?”

Bridge to Article 3:

Once we understand the fault lines, the reform agenda becomes clearer. Article 3 proposes a practical roadmap for 2026–2035: minimum protection, informal-worker contribution design, lifelong-income defaults, EPS improvements with funding clarity, portability, and transparent public pension costing.

REFERENCES — ARTICLE 2

India’s Pension System Today: Who Gets What—and Why Many Pensions Stay Small

India’s Pension Architecture

- Pension Fund Regulatory and Development Authority (PFRDA)

National Pension System (NPS): Annual Reports & Scheme Guidelines

– Structure, investment norms, exit rules, and scale of NPS. - Ministry of Finance – Department of Financial Services (DFS)

Atal Pension Yojana (APY) Dashboard & Scheme Guidelines

– Subscriber numbers, contribution slabs, and benefit design. - Employees’ Provident Fund Organisation (EPFO)

EPF & EPS Scheme Documents and Annual Reports

– Formal-sector retirement savings and pension structure. - Press Information Bureau (PIB), Government of India

Cabinet Approvals and Official Releases on Pensions

– Unified Pension Scheme (UPS), CPPS rollout, social security coverage updates.

Coverage & Adequacy Evidence

- International Labour Organization (ILO)

World Social Protection Report 2024–26

– Pension coverage, adequacy gaps, and global benchmarks. - Economic Times / Business Standard (based on Parliamentary & EPFO data)

– Reporting on EPS pension distribution and adequacy concerns. - Reserve Bank of India (RBI)

State Finances: A Study of Budgets

– Pension-related fiscal pressures at Centre and State levels.