India’s China+1 Moment: From iPhones to Fighter Jets

Amulya Charan – July 2026

1. Introduction

For the better part of two decades, “made in China” was not so much a label as the operating system of global manufacturing. Circuit boards, stitched seams, motors, casings, chargers and final assemblies all seemed to converge somewhere in the Pearl River Delta, the Yangtze River Delta or the wider supplier network that feeds them.

That system is not disappearing. China remains the world’s deepest manufacturing base. What has changed is the risk calculation. Companies and governments that once optimized almost entirely for Chinese efficiency now pay for redundancy.

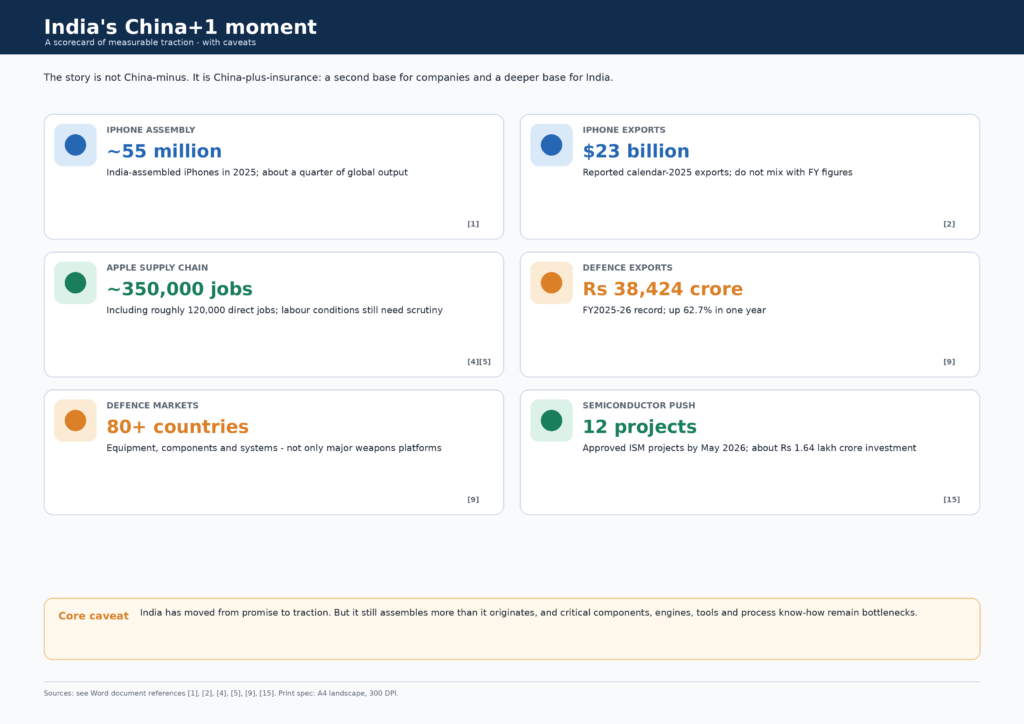

That is the useful way to read India’s China+1 moment. It is not China-minus. It is China-plus-insurance. The aim is not to replace China overnight, but to make sure that a tariff, lockdown, export-control decision, shipping disruption or diplomatic crisis cannot freeze an entire product line. On that narrower test, India’s case is stronger than at any earlier point in the past three decades.

The evidence has moved from consultancy slides to export ledgers, factory payrolls, defence order books and semiconductor construction sites. The right conclusion is not that India has arrived at the top of the value chain. It has not. The better conclusion is that India has become a serious manufacturing node – and that the next decade will decide whether assembly turns into component depth, process ownership and technology leverage.

Figure 1. References [1], [2], [4], [5], [9] and [15].

2. The iPhone is the cleanest signal

Begin with the product that has become the most visible gauge of the shift. Industry estimates reported in early 2026 put Apple’s India output at about 55 million iPhones in calendar 2025, up from 36 million in 2024, or roughly a quarter of global iPhone production. [1] That figure should be described as an estimate, because Apple does not publish country-by-country production numbers. But even with that caveat, the scale is hard to dismiss.

As recently as 2020, India’s role in iPhone assembly was marginal. Moving from a rounding error to something near one in four units within a few years is not a token hedge. It is a re-engineering of one of the most finely tuned consumer-electronics supply chains ever built.

What moved Apple was not sentimentality about India. It was risk. The late-2022 disruption at Foxconn’s Zhengzhou complex exposed the cost of concentrating too much premium iPhone output in one Chinese location at the wrong moment. The diversification that followed was less ideology than a board-level response to a visible operational shock.

The export ledger shows the same turn. In calendar 2025, iPhone exports from India were reported at about $23 billion, making the iPhone the country’s most valuable product-level export in that year. [2] A fiscal-year lens is slightly different: for the year ended March 2025, smartphone exports topped $23 billion, including more than $17 billion in iPhones. [3] The distinction matters. Calendar-year and fiscal-year figures should not be mixed.

The jobs story is also real, but it needs guardrails. Reporting citing officials put Apple’s expanded India supply chain at about 45 companies and roughly 350,000 jobs, including about 120,000 direct jobs. [4] Women account for a large share of electronics assembly work, and formal factory employment for young women can matter deeply in a country that needs millions of new jobs each year. But this should not be written as a simple triumphal line. Labour practices, transport, hostels, overtime, contractor systems, grievance channels and anti-discrimination compliance need scrutiny. Reuters-reported allegations about hiring discrimination against married women at a Tamil Nadu iPhone plant led India’s labour ministry to seek a state investigation; Apple and Foxconn denied discrimination. [5]

The local-company point is important, too. Tata Electronics’ expanding role in Apple’s India ecosystem suggests that Indian operating capability is growing, not merely that foreign contractors are renting inexpensive labour. But the claim should stop there. To say knowledge is being absorbed requires evidence of component localization, supplier qualification, process engineering, management depth and eventually design ownership. India’s challenge is to move from final assembly toward the harder layers of the supply chain.

3. One company’s hedge becomes everyone’s playbook

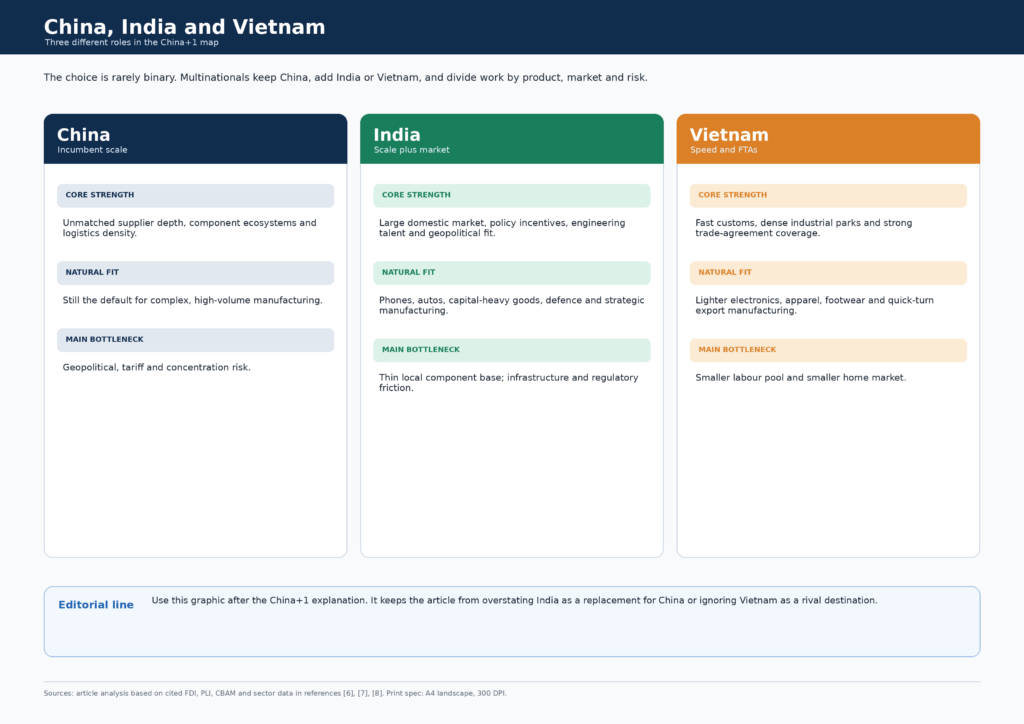

Treat Apple as a one-off and the larger pattern disappears. The basic China+1 idea is simple: keep China because its capabilities remain too deep to abandon, but build a second production home so that one country’s politics, pandemic policy, tariff regime or logistics disruption cannot cut off customers.

By 2026, this is no longer a niche risk-management discussion. It is a mainstream boardroom question. The US-China trade fight is one driver. Pandemic memory is another. Europe adds a different kind of pressure through the Carbon Border Adjustment Mechanism. CBAM is not a rule against single-origin supply chains; it is a carbon-pricing and reporting regime for the embedded emissions in selected carbon-intensive imports such as cement, iron and steel, aluminium, fertilisers, electricity and hydrogen. [6]

India’s pitch rests on several pillars: a large domestic market, a wide engineering base, English-language managerial talent, policy subsidies, and geopolitical comfort with Washington, Brussels, Tokyo, Canberra and Abu Dhabi. The investment numbers also look stronger than in earlier cycles. Provisional gross FDI inflows reached $81.04 billion in FY2024-25, up 14%, while manufacturing FDI rose 18% to $19.04 billion. [7]

The Production Linked Incentive scheme is a visible part of this turn, but the numbers should be handled carefully. Government figures reported to Parliament put actual investment realized under the 14 PLI schemes at Rs 1.76 lakh crore by March 2025, with production and sales above Rs 16.5 lakh crore. [8] Higher figures may exist for commitments or approvals, but they should be labelled as such.

India is not the only winner. Vietnam is a formidable rival for lighter and faster-turnover manufacturing, helped by speed, export discipline, industrial-park density and free-trade agreements. India has a different pitch: market scale, labour depth, policy money and the ability to absorb capital-heavy sectors such as phones, autos, defence and semiconductors. Above both sits China, still unmatched on supplier depth and logistics. That is why the right frame is not replacement. It is diversification.

Figure 2. I Phone Exports.

4. Defence: Export momentum with limits

Defence is the same instinct in a different vocabulary. In corporate language, the goal is supply-chain resilience. In national-security language, it is strategic autonomy.

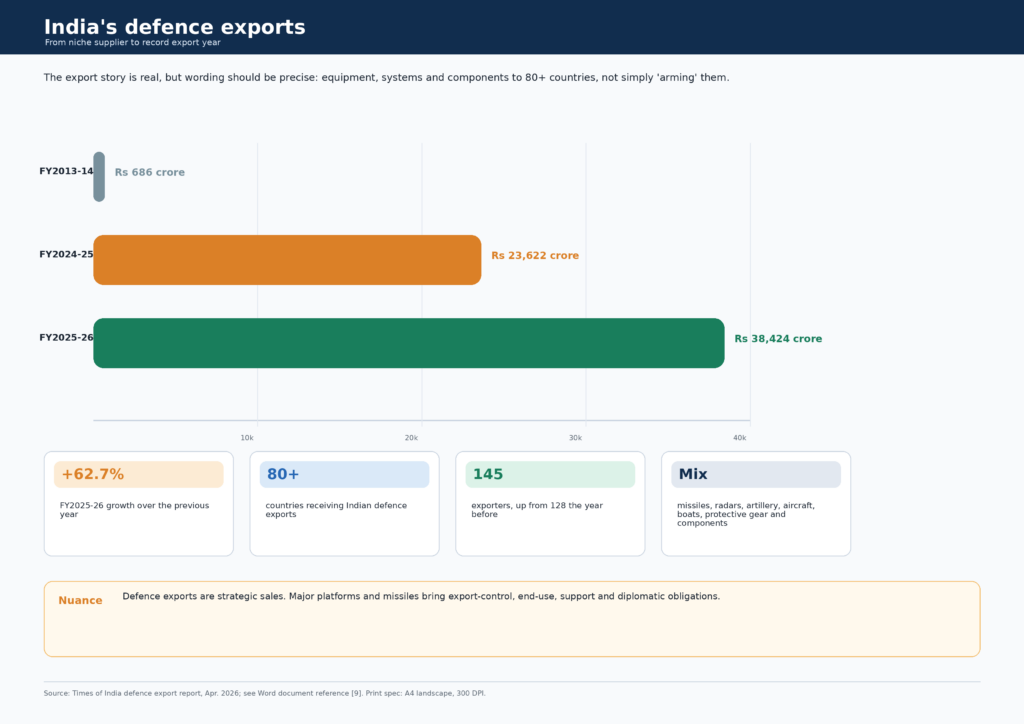

India’s defence exports touched Rs 38,424 crore in FY2025-26, up 62.7% from Rs 23,622 crore the previous year, with shipments to more than 80 countries. [9] That is a record and it deserves attention. But wording matters. India is not suddenly “arming eighty countries” with major platforms. It is exporting a mix of defence equipment, components, systems and services, including missile systems such as BrahMos, radars, artillery, electronic-warfare systems, armoured vehicles, Dornier-228 aircraft, boats, protective gear and other items. [9]

Domestic defence output has scaled as well, reaching a reported Rs 1.78 lakh crore in FY2025-26, up from Rs 1.54 lakh crore the previous year. [10] The direction is clear: India is trying to become not only a large defence buyer, but a larger defence producer and selective exporter. The harder question is how much of that production rests on Indian intellectual property and critical subsystems.

Figure 3. Defence-export opening, See reference [9].

5. The Tejas lesson: a real platform with a foreign engine

The Tejas light combat aircraft captures both the achievement and the limit. It is a real Indian fighter programme with a growing production base and large domestic orders. But the Mk1A depends on GE Aerospace’s F404 engine. That dependence became visible when engine deliveries ran late. HAL imposed contractual penalties on GE; by April 2026, reporting said GE had committed to supply 20 engines by December 2026 and that a sixth engine was expected by the end of April. [11]

That is not a solved bottleneck. It is a recovering bottleneck. The distinction matters because export ambition depends on production confidence. Any foreign sale of Tejas also has to reckon with the approvals and timelines attached to US-origin engines and other imported content. The lesson generalizes beyond one aircraft: standing up an assembly line is difficult, but mastering the engine, the hot section, the sensor, the chip or the process technology is the long climb.

6. BrahMos: export momentum, not just a headline

BrahMos points to the upside when a complex Indian-linked system finds external demand. The Philippines opened the export account with a $375 million shore-based anti-ship missile order. By May 2026, India’s defence secretary said a BrahMos deal with Vietnam had been signed and that an Indonesia pact was in final stages. [12]

That points to genuine export momentum in Southeast Asia, particularly among states watching maritime pressure in the Indo-Pacific. But missile exports are not normal commercial sales. They bring end-use commitments, export-control decisions, training, spares, maintenance, software support and diplomatic management. The export franchise will depend as much on after-sales credibility as on the headline contract value.

7. Silicon is the hardest exam

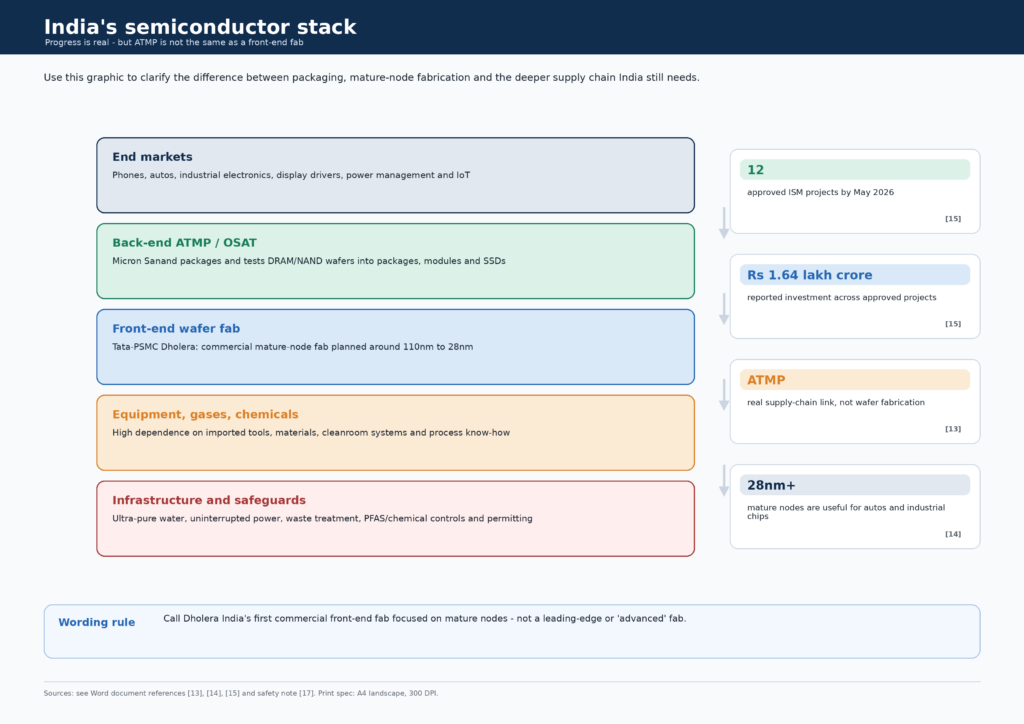

The phone and defence stories both hide the same dependency in plain sight: chips. India designs software and consumes semiconductors at enormous scale, but for decades it made very few of the chips it used. The new semiconductor push matters because it has finally moved from policy promise to physical facilities.

Micron’s Sanand project is the cleanest example of progress with a caveat. It is an ATMP facility – assembly, testing, marking and packaging – rather than a front-end wafer fab. It will receive DRAM and NAND wafers from Micron’s global fabs and convert them into packages, modules and SSDs. [13] That is a real supply-chain link and a meaningful first step. It is not the same as making the wafer itself.

The front-end bet is Tata Electronics’ Dholera fab with Taiwan’s PSMC. The plant is described as India’s first commercial front-end fab, backed by about Rs 91,000 crore, and planned around mature-node processes from 110nm to 28nm at up to 50,000 wafers a month. [14] It should not be called a leading-edge fab. The newest phone processors are made at much smaller nodes. But mature nodes are not second-rate business. They power cars, industrial electronics, display drivers, power-management chips and many connected devices. For a newcomer, they are the logical place to learn yield, reliability, vendor qualification and customer discipline.

The ecosystem is widening. As of May 2026, public reporting put India at 12 approved semiconductor projects under the India Semiconductor Mission, with investment of about Rs 1.64 lakh crore. [15] That is a cleaner figure than looser project counts unless the scope is defined. The risks now are operational: water, power, cleanroom skill, equipment uptime, chemical handling, waste treatment, environmental compliance and the local vendor base.

Figure 4 : ATMP, mature-node fabrication and ecosystem constraints. References [13]-[15] and [17].

8. The uncomfortable middle of the value chain

The part that should not be hidden is also the part that makes the story credible: India still assembles far more than it originates. Many components in its phones, many critical parts in its defence platforms and much of the equipment inside its fabs are imported. Some of the most important inputs still come directly or indirectly from China.

That is why selective easing around Press Note 3 is not a contradiction. It is an admission of where the value chain stands. Recent reporting said India had relaxed some approval rules for investments from land-border countries in selected sectors such as capital goods, electronics and solar cells, including a 60-day decision timeline for certain proposals. [16] The point is not a wholesale reopening to Chinese capital. It is a security-screened attempt to bring in the capital, machinery and technical partnerships needed to deepen manufacturing.

This is the arithmetic of catch-up. China+1 does not mean every component is made outside China immediately. It means the final assembly, some supplier qualification, some process knowledge and eventually some deeper local sourcing begin to migrate. India is somewhere in the middle of that journey.

9. What to watch next

- iPhones: Does India’s assembly share keep rising, and does component localization rise with it rather than leaving India mostly at final assembly?

- Jobs: Do electronics plants create durable formal employment while improving transport, hostels, overtime controls, contractor governance and anti-discrimination safeguards?

- Tejas: Do GE engine deliveries stabilize enough for HAL to meet domestic schedules before promising exports?

- BrahMos and defence: Do export deals translate into repeat orders, reliable after-sales support and deeper Indian subsystem content?

- Semiconductors: Does Dholera produce first silicon and then prove yield, reliability and customer qualification at scale?

- Press Note 3: Does selective easing build component depth without creating new security or dependency risks?

10. The better conclusion

India’s China+1 moment has moved from promise to traction. It is visible in iPhones exported by the billions of dollars, defence equipment shipped to dozens of countries and semiconductor plants that are now physical projects rather than policy slogans. But traction is not the same as transformation.

The next questions are simple and unforgiving. Can India move from assembling phones to making more of their components? Can it turn defence production into technology ownership, not just licensed or imported subsystems? Can it build fabs that do not merely open, but run reliably, qualify customers and manage environmental obligations? Can it use Chinese capital and equipment selectively without recreating the dependency it is trying to reduce?

India has earned a place in the China+1 conversation. It has not yet earned the right to declare the climb complete. The more durable story is also the more accurate one: India is no longer just promising to become a manufacturing alternative. It is becoming one, unevenly and with real constraints, but on a scale the world can no longer ignore.

11. References

Reference markers in the article correspond to the sources below. Titles are clickable links in the Word document.

[1] Times of India, “iPhone production in India jumps 53% in 2025; Apple now assembles all versions of iPhone in the country”, 10 Mar. 2026. Used for: India iPhone production estimates: 55 million units, roughly 25% of global output.

[2] Economic Times, “India’s iPhone exports hit $23 billion in 2025 as smartphones become top export segment”, 23 Feb. 2026. Used for: Calendar-2025 iPhone export figure and product-level export claim.

[3] Wall Street Journal, “India Saw a Surge in Smartphone Exports in Recent Months Ahead of Tariffs”, 11 Apr. 2025. Used for: Fiscal-year distinction: smartphone exports above $23 billion, including more than $17 billion in iPhones.

[4] Economic Times, “As Apple spreads its branches, 45 companies now plugged into Indian supply chain”, 28 Sep. 2025. Used for: Apple India supply-chain employment and supplier expansion.

[5] The Times, “Apple’s biggest phone supplier denies bias against married women”, 27 Jun. 2024. Used for: Labour nuance: investigation request and company denials following Reuters-reported allegations.

[6] European Commission, “Carbon Border Adjustment Mechanism”, Official page, accessed Jun. 2026. Used for: Correct description of CBAM as embedded-carbon reporting/pricing for specified sectors.

[7] Economic Times, “India records $81.04 bn FDI inflow in FY25”, 27 May 2025. Used for: Gross FDI inflows, manufacturing FDI, and cumulative FDI figures.

[8] Economic Times, “Rs 21,534 crore incentives disbursed under 12 PLI schemes till June 24: Govt to Parliament”, 22 Jul. 2025. Used for: PLI actual investment realized, output and incentive disbursement figures.

[9] Times of India, “Defence exports skyrocket to record Rs 38,424cr in 2025-26”, 3 Apr. 2026. Used for: FY2025-26 defence export record, growth rate, export destinations and product mix.

[10] Economic Times, “Doubled in 5 years: India’s military-industrial moment has arrived”, Jun. 2026. Used for: Domestic defence production estimate for FY2025-26.

[11] Times of India, “HAL imposes contractual penalties on GE for Tejas engine delivery delay”, 4 Apr. 2026. Used for: Tejas Mk1A engine-delivery delays and GE delivery commitments.

[12] Times of India, “BrahMos deal with Vietnam signed, missile pact with Indonesia in final stages”, 30 May 2026. Used for: BrahMos export momentum in Southeast Asia.

[13] Times of India, “PM to inaugurate Micron’s ATMP plant in Sanand on Saturday”, 27 Feb. 2026. Used for: Micron Sanand as ATMP: packaging/testing DRAM and NAND wafers, not front-end fabrication.

[14] Tom’s Hardware, “ASML partners with Tata Electronics to equip India’s first commercial semiconductor fab”, 17 May 2026. Used for: Dholera fab: mature-node range, wafer capacity, investment and target applications.

[15] Times of India, “Gujarat’s semiconductor sector gets Rs 3,900cr push for two units”, 6 May 2026. Used for: 12 approved ISM projects and cumulative investment estimate.

[16] Times of India, “Govt relaxes FDI investment rules from China, other neighbouring countries”, 10 Mar. 2026. Used for: Selective easing around Press Note 3 approvals for some sectors and timelines.

[17] arXiv, “Modeling PFAS in Semiconductor Manufacturing and Electronics”, 2025. Used for: Environmental/safety context for PFAS and fluorinated chemicals in electronics and semiconductor manufacturing.

————————————————————————————————————————————

Amulya Charan writes on energy systems, infrastructure economics, and development policy at amulyacharan.com.