Environmental Finance in India and Beyond

Green Bonds · ESG Investing · Climate Capital

1. Introduction

Environmental finance — a suite of financial instruments and market-based mechanisms aimed at funding climate and sustainability initiatives — has rapidly risen in importance. Among emerging markets, India stands at the forefront, developing instruments like green bonds, embracing ESG investing, and mobilizing climate capital initiatives. However, India’s journey is best reflected in comparison to global peers (China, US, EU, Brazil, etc.), underscoring both strides made and gaps to fill.

2. Green Bonds

2.1 What Are Green Bonds?

Labelled debt instruments exclusively funding projects with positive environmental impacts—renewable energy, clean transport, water conservation, and more—green bonds typically follow frameworks like the ICMA Green Bond Principles. They aim to channel capital to climate-positive outcomes while offering investors a “greenium” (price premium for green labelling) theprint.in.

2.2 Global Green Bond Landscape

- Global green bonds issuance surpassed US$2 tn by Q3 2022 climatebonds.net.

- China and the US jointly account for ~60% of global volume, with China recently becoming the top issuericmagroup.org+3sciencedirect.com+3energytracker.asia+3.

- Europe contributed 53% of aligned green bonds in 2023 (~US$310 bn), with North America’s share shrinkingft.com+3climatebonds.net+3climatebonds.net+3.

2.3 India’s Green Bond Progress

- Since the first issuance in 2015 (Yes Bank green masala bond), India’s cumulative green, social, sustainability (GSS+) debt has soared to US$55.9 bn by Dec 2024, up 186% from 2021broadridge.com+3climatebonds.net+3theprint.in+3.

- 83% of India’s GSS+ issuance is green-labelled—a higher proportion than many peersen.wikipedia.org+11climatebonds.net+11ieefa.org+11.

- India ranks second among emerging markets (after China) in green bond issuance volume icmagroup.org.

2.4 Sovereign & Municipal Green Bonds

- India’s first sovereign green bonds were issued by RBI in renegotiable form (~INR 477 bn).

- Municipal bonds, like Pimpri Chinchwad and Nashik, illustrate growing investor interest (oversubscribed issues, 7–8% yield) .

2.5 Corporate Issuances in India

- Adani Green Energy (SGX‑listed, US$362.5 mn), L&T (₹500 cr ESG bond at a price premium) .

2.6 Challenges & Outlook

- Depth concerns: Sovereign green auctions have seen significant devolvement and yield spreads requiring deeper demand .

- Scaling up: India requires US$68 bn/year for renewables (current ~US$13 bn) .

- Greenwashing risk: Calls for unified taxonomy, stricter impact verification and consistent reporting .

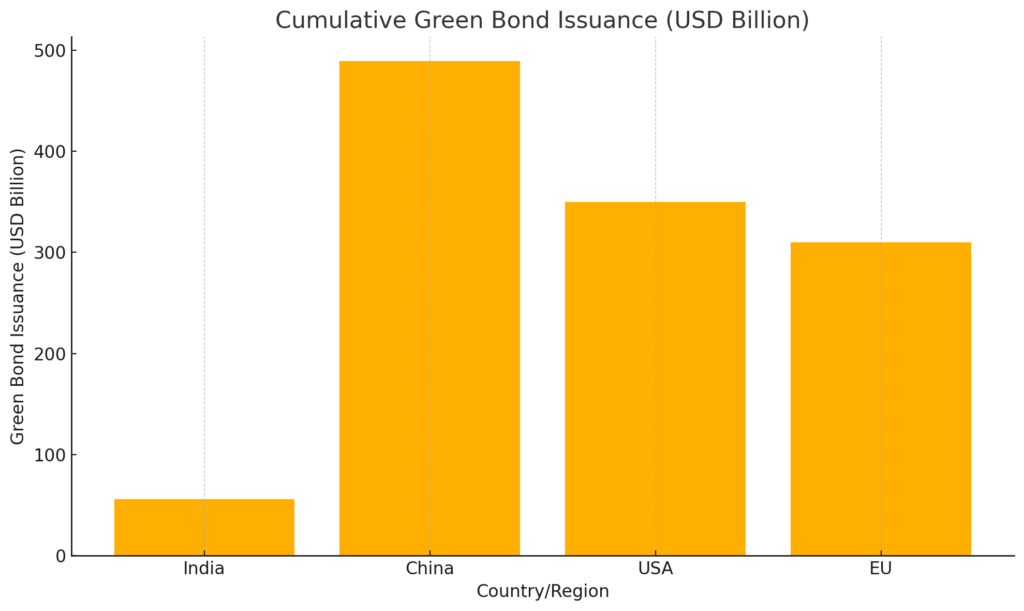

2.7 Comparison with Other Economies

| Country / Region | Cumulative Green Bond Issuance | % of Global Issuance | Taxonomy & Oversight |

| China | ~US$489 bn (by 2022) | Largest single market – ~30%–35% | PBoC guidance, exclusion of LGF |

| United States | US$300–400 bn/year; top in 2020 | 11% of global sustainable funds | Voluntary standards, more greenwashing scrutiny |

| Europe | ~53% of aligned issuance in 2023 (~US$310 bn) | Leading region on ESG integration | Europe-wide taxonomy, EUGB standard since 2024 |

India trails in sheer volume but shines in emerging-market context. With taxonomy underway, India is aligning more with global standards.

3. ESG Investing

3.1 What is ESG Investing?

ESG investing combines traditional financial metrics with Environmental, Social, and Governance (ESG) factors—fostering capital allocation that aligns with sustainability goals and responsible investment practicesbroadridge.com+7reuters.com+7ieefa.org+7.

3.2 Scale & Trends: India vs Global

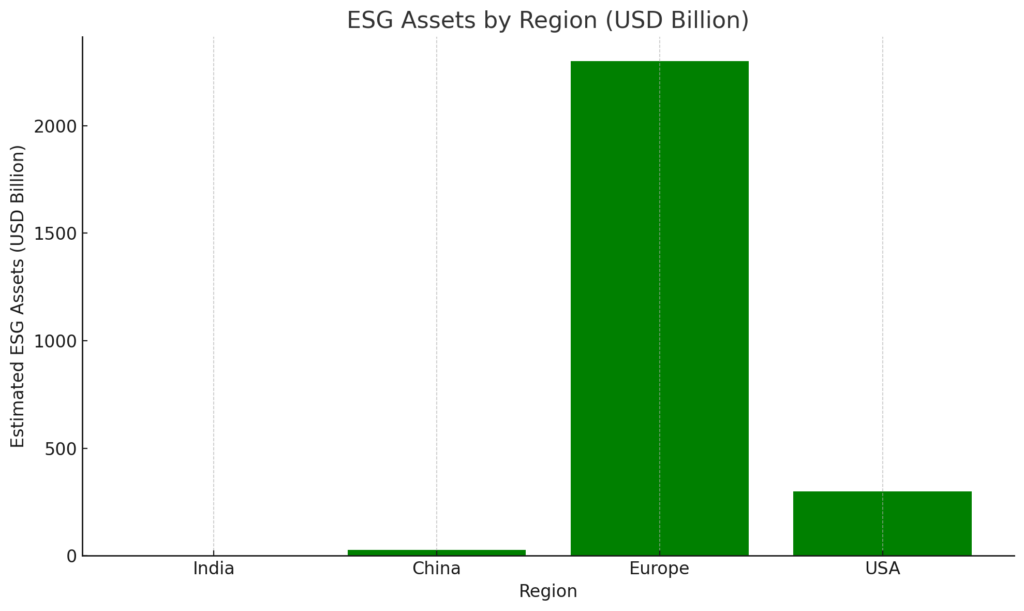

- India’s ESG assets stood at ~US$1.22 bn in 2024, projected to reach US$4.11 bn by 2030 (23% CAGR) .

- This accounts for ~4.3% of India’s share in the global ESG market (2024) .

- By contrast, Europe holds 84% of global sustainable fund assets (~US$2.3 tn); the US has ~11% (~US$300 bn) .

3.3 Drivers & Institutional Push

- Regulation: SEBI mandates Business Responsibility and Sustainability Reports (BRSR); labels for ESG mutual funds.

- Retail enthusiasm: Younger investors seek ESG-aligned options (India’s ESG 2.0) .

- Global asset managers, including those from Europe and US, allocating to India under ESG mandates .

3.4 Challenges Facing ESG Investing in India

- Limited product ecosystem: India has fewer standalone ESG funds compared to top-10 economies reuters.com.

- Data and transparency: 39% of North American companies fail to report climate data vs. 13% in Europeinrate.com, indicating scope for India.

- Greenwashing risk: Globally rife, especially in the US where scrutiny is high .

3.5 Comparative ESG Trends

- Europe: Well-established ESG funds (5,600+ funds, €2.3 tn); stringent reporting .

- US: First-quarter 2025 saw US ESG funds face record outflows (~US$8.6 bn), political backlash and policy uncertainty .

- China/Japan: ESG assets tripled post‑2020; China’s clean energy funds ~$26 bn; Japan’s ESG investing closing in on EU levels .

3.6 Returns & Future Outlook

- Global sustainable funds outperformed traditional peers in 2023: median returns of 12.6% (ESG) vs 8.6% (traditional) ieefa.org.

- India’s asset growth prospects remain strong, helped by intensifying ESG regulations, improving BRSR compliance, and rising investor demand .

4. Climate Capital & Sustainable Finance Instruments

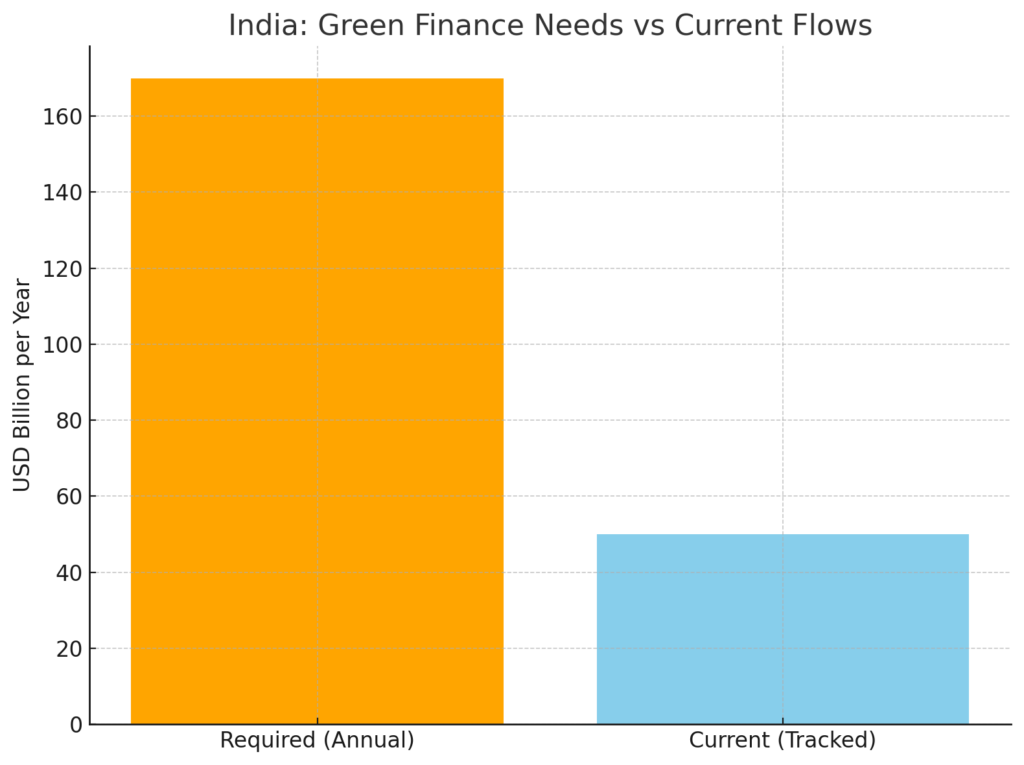

4.1 Scale of Financing Needs

- India’s NDC and net‑zero targets require ~US$2.5 tn by 2030 (~US$170 bn/year), including ~US$1 tn in adaptation .

- Current tracked green finance is ~INR 3.7 tn (~US$50 bn/year)—35–40% short of target .

4.2 Funding Sources

- Domestic flows make up ~83% of green finance—66% private, 17% public .

- Project financing via banks, ESG-linked bonds, loans (e.g. GIFT City), and equity from climate tech and renewables.

4.3 Major Players

- NIIF and its Green Growth Equity Fund (“GGEF”) catalyse sustainable infrastructure.

- DFIs (World Bank, ADB), public sector banks, PSU treasuries, asset managers, and PE/VC funds supporting climate ventures.

4.4 Innovative Instruments

- ESG‑linked transition bonds in GIFT City: coupon tied to sustainability KPIs .

- Sustainability-linked loans/bonds: growing, but with calls for stronger covenants.

- Blended finance: combines grants/guarantees with private investment; risk-reduction models emerging.

4.5 Comparison with Global Blended Finance

- EU: NextGenerationEU uses green bonds (~30% of €750 bn plan) .

- China: combines ESG bonds with carbon trading—now covering ~40% of emissions .

- US: LOCKED by policy uncertainty; yet clean-tech financing (electric vehicles, grids) still strong (~US$22 bn in 2025) ft.com.

5. Policy, Taxonomy & Regulation

5.1 India’s Climate Finance Taxonomy

Work in progress. Aims for clear definitions covering activities aligned with national targets; aligned with international standards .

5.2 Financial Regulation

- RBI: sovereign green bond issuance; guidelines forthcoming.

- SEBI: mandatory BRSR disclosures and ESG fund standards; investor-centric labelling.

- IFSCA: ESG‑linked bond framework in GIFT City theprint.in.

5.3 Policy Gaps & Recommendations

- Harmonize taxonomy with Global South alignment and EU benchmarks.

- Strengthen municipal green bond issuance with technical support and credit guarantees.

- Introduce fiscal incentives: risk-sharing, interest rate subvention, tax breaks for green capital.

6. Comparative Snapshot

| Dimension | India | China | Europe | United States |

| Green Bond Volume | US$56 bn cumulative (GSS+) | US$489 bn (by 2022)fnlondon.com+3en.wikipedia.org+3icmagroup.org+3climatebonds.net+1energytracker.asia+1 | US$300 bn+ aligned (53% share in 2023) | US$300–400 bn $/year (~11% share) |

| ESG Asset Base | US$1.2 bn (4% market share) | US$26 bn (clean energy AUM) | US$2.3 tn; 5,600+ funds | US$300 bn; facing outflows |

| Taxonomy/Regulation | Draft taxonomy; SEBI/IFSCA frameworks | PBoC standards; national carbon ETS (~40% emissions) | EU Taxonomy & EUGB Regulation (since Dec 2024) | Voluntary regs; backlash & state-level ESG restrictions |

| Capital Need | US$170 bn/year to meet NDCs | US$ hundreds of bn annually in renewable transition | EU Green Deal target €1 tn by 2030 | IRA & Inflation Reduction Act drive US$22 bn cleantech in 2025 |

7. Key Challenges & Opportunities

7.1 India’s Bottlenecks

- Financing gap (~60–70% of target unmet).

- Smaller ESG product range and limited retail participation.

- Weak data infrastructure, especially at provincial & municipal levels.

- Greenwashing concerns, given absence of unified taxonomy.

7.2 Aligning with Global Momentum

- European regulatory rigor offers a model—taxonomy, labelling, fund structures.

- China’s ETS and bond standard frameworks show integrated policy-finance ecosystem.

- US cleantech financing demonstrates how policy incentives can drive massive flows, despite political flux.

7.3 India’s Strategic Opportunities

- Expand sovereign and municipal green bond issuance, anchoring yield curve and market liquidity.

- Build ESG fund ecosystem, backed by tax incentives and public awareness.

- Foster blended finance partnerships, integrating DFIs and local financing to mitigate risk.

- Adopt standardized taxonomy & audit, aligned globally.

8. Case Studies

8.1 Pimpri-Chinchwad Municipal Green Bond

- ₹200 cr at 7.85%; 5× oversubscription—proof of strong investor demand fnlondon.comtheprint.in.

8.2 Adani Green Energy (Offshore)

- US$362.5 mn bond on SGX—India’s landmark offshore issuance .

8.3 EU NextGenerationEU Green Bonds

- Up to 30% of €750 bn recovery fund funded via green bonds; EUGB in effect December 2024 .

9. Visual Data Summary

- Emerging Market Green Bond Issuance (India 2nd to China) .

- Asia-Pacific Growth (China, Japan, Korea surge) spglobal.com.

- China SOE vs Financial Corporate Bonds (48/52 split) .

- Green Bonds Milestones globally (2015–2022) .

10. The Road Ahead

Growth Strategies

- Scale sovereign & municipal issuance to serve as benchmarks.

- Incentivize private ESG funds; expand retail channels.

- Standardize data, reporting, taxonomy.

Innovation & Governance

- Adopt ESG-linked bond markets and KPIs.

- Embed environment in central financial policy.

- Encourage disclosure through BRSR and sustainable product certification.

Building Bridge Capital

- Use guarantees, blended finance structures.

- Promote investable pipelines with de-risking.

- Integrate carbon markets, carbon credits, and climate risk insurance.

11. Conclusion

India’s environmental finance journey shows promise but remains at a pivotal stage. Instruments like sovereign green bonds, ESG regulations, and private-sector engagement provide solid foundations. Yet, to match advanced and emerging global peers (China, EU, US), India must deepen finance, formalize oversight, expand product ecosystems, and channel capital at scale—bringing trillions of dollars behind its carbon-constrained growth path.

If India succeeds, it can emerge as a global leader in sustainable finance—a beacon for emerging economies navigating the green transition.

Next Steps & Implementation Ideas

- Stakeholder Workshops: collaborate with SEBI, RBI, think-tanks on taxonomy.

- Pilot ESG Funds: target retail adoption; integrate with SIPs, pensions.

- Capacity Building: for municipal bodies in bond issuance.

- Global Engagement: leverage DFIs, diaspora investment, climate funds.

Congratulations for an excellent writeup summarising an extremely complex landscape, with quantitative comparisons between India and developed countries.

Thanks