How Energy Inflation Erodes Retirement Savings

Pension Series · Part 5

Fifth in our series on whether Indians are saving enough for old age. Earlier parts mapped the system (Part 1), the coverage gap (Part 2), the choice between guaranteed and market-linked products (Part 3), and the habits that quietly sabotage a saver (Part 4). All four were, in the end, about how much you put away. This one is about how fast it leaks out once you stop earning — and why the price of energy is doing more of the leaking than most retirement plans ever account for.

1. Why your pension corpus is smaller than it looks

Open any retirement account and your eye goes straight to one number: the corpus. The lakhs, the crores, the figure you spent a working life assembling. It looks like an achievement, and it is. But it is also a trick of the light. That number is in today’s rupees, and you will be spending it in tomorrow’s. What matters is not how large the pile is but how much it will actually buy in 2040, or 2050, when you are drawing it down a thousand rupees at a time.

That gap — between what the statement says and what the money does — is the whole subject of this article. Inflation is what opens it. And of all the things that inflate, energy is among the most punishing, for reasons we will get to. You did not have to take my word for any of this in the early summer of 2026. A standard cooking-gas cylinder in Delhi had been nudged past ₹940, petrol and diesel were up several rupees a litre inside a few weeks, and anyone living on a fixed monthly income could feel the arithmetic tightening around them in real time.

2. The series so far, and the thing it skipped

A quick orientation for anyone joining late. India’s retirement system is less a system than a collection of schemes that never quite agreed to work together. There is the Employees’ Provident Fund and its attached pension scheme for organised private-sector workers. There is the National Pension System, market-linked and run by the PFRDA, which had grown to roughly ₹15.95 lakh crore in assets by the end of March 2026. There is the Atal Pension Yojana for lower-income and informal workers, the small-savings schemes that retirees lean on for safety, and a separate, much-argued-over arrangement for government staff.

The thread running through the first four articles was a simple, uncomfortable finding: the formal schemes between them reach fewer than one in four Indian workers, one of the thinnest coverage rates of any large economy. And where people are covered, the benefits are often modest. The Mercer–CFA Institute’s global pension ranking has parked India near the very bottom of the countries it scores, with its weakest mark on the measure that matters most in the end — adequacy, the plain question of whether retirees get enough to live on.

Adequacy is where we pick up. The earlier pieces treated it as a design problem: contribute more, invest better, behave sensibly. Fair enough. But a pension is a promise about the future, and the future arrives with its own price tag. Inflation is the biggest reason a plan that pencils out today can fall apart tomorrow, and energy is one of the loudest voices inside inflation. That it has barely featured in the Indian retirement conversation is, frankly, an oversight worth correcting.

3. India pension inflation: the headline rate is not your rate

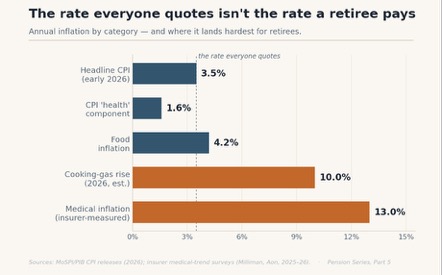

For most of early 2026 India’s official retail inflation behaved itself, drifting around 3.5% a year and sitting comfortably below the Reserve Bank’s 4% target. Reassuring, if you stop reading there.

You should not. The headline number is an average, and averages are built from a basket meant to describe a typical household. A retiree is not typical. Older people pour most of their money into a short list of things they cannot do without — food, rent, medicine, fuel, power — and almost none into the cars, gadgets and holidays where prices have lately gone soft. When the items dragging the average down are things you never buy, the official figure is quietly lying to you. Not maliciously. Just structurally. It is why so many retirees insist they feel poorer than the data says they should be. They are right, and the data is averaging away their reality.

There is a deeper hole here, too. India does not publish a price index for the elderly at all. A few countries track what older people actually spend on; India simply hands every pensioner the same average and wishes them luck.

Figure 1 — The rate everyone quotes is not the rate a retiree pays.

The medical inflation no index will tell you about

Health is where the gap turns from inconvenient to dangerous, and for a retiree health is not some line item to be optimised — it is the line item. Here the official CPI prices health at well under 2% a year. Meanwhile the people who actually settle the bills, the insurers, put medical inflation at somewhere around 12 to 14% a year through 2025–26, among the steepest in Asia. A ₹5 lakh procedure today is on track to cost closer to ₹9 lakh within five years at that pace.

For someone still working, with a salary and an employer’s group cover, that is an annoyance. For a retiree — older, more likely to need treatment, far more likely to be paying out of their own pocket, and living on an income that does not grow — it is one of the central financial risks of the rest of their life. And the headline number renders it nearly invisible.

4. Why energy hits a pension harder than almost anything

Energy reaches a retiree by two roads. The obvious one is the bill itself: the cylinder, the electricity meter, the petrol if there is still a scooter in the family. None of it is optional. You cannot cook less gas or sweat through an Indian May without a fan, so when these prices climb the household just absorbs the hit — by trimming something else, or by dipping into savings a little faster than the plan allowed.

The road that does the real damage is the quieter one. Energy is baked into the price of nearly everything. The vegetables at the market carry the diesel that drove the tractor, the truck that brought them in, the cold store that kept them from spoiling. Medicines, bus fares, a plumber’s call-out, a packet of biscuits — each has an energy cost folded inside it. So when fuel jumps, the shock does not stay in the fuel column. It seeps, with a lag, into the price of things that have nothing obviously to do with oil. A retiree who walks everywhere and cooks like a monk still cannot dodge energy inflation. It finds them through the grocery bill.

Put those two roads together and you see why energy and the pension problem are so tightly bound. Think of the corpus as a tank that has to last thirty years on a slow drip. Energy inflation does not raise one tap; it widens the whole drain. And the retiree, unlike the salaried worker who can ask for a raise or pick up extra work, is holding a fixed claim. The number does not move. The cost of living does.

5. The 2026 energy shock, as a live stress test

For a decade this was mostly theory for Indian savers. Prices wobbled, but nothing broke. Then 2026 turned the theory into something you could watch on the news.

Conflict in West Asia choked shipping through the Strait of Hormuz, the narrow neck of water that a vast share of the world’s seaborne energy has to pass through. India is badly exposed there. It imports the great bulk of the crude it burns and most of its cooking gas, and by the government’s own reckoning more than half of that LPG comes through the Strait. When the lane clogged, global fuel prices lurched upward, and the lurch did not stay offshore.

It landed in kitchens within weeks. A 14.2 kg domestic cylinder in Delhi was marked up twice in 2026 — a bigger rise in March, another in early June — carrying the price past ₹940 for the ordinary buyer. Petrol and diesel went up by a cumulative ₹7.50 a litre in short order. Piped and compressed gas climbed as well. Individually, small numbers. Stacked, and feeding into food and transport through that quiet second road, they added up to something an older household felt sharply: the same pension, buying visibly less.

The point is not really the war. Wars end. The point is that energy is structurally volatile and politically exposed in a way that rice and rent usually are not. A retirement plan does not have to survive an average decade. It has to survive the bad years buried inside the average — and energy is reliably where the bad years come from.

6. The math of erosion

The intuition undersells the damage, so look at the numbers instead.

Inflation compounds, and compounding does its ugliest work over the twenty-five or thirty years a modern retirement can run. At a steady 6%, prices roughly double every twelve years. A lifestyle that costs ₹50,000 a month at sixty needs about a lakh a month by seventy-two, and something near two lakh by the mid-eighties — same life, same modest comforts, triple the rupees. Nobody made a mistake. The calendar simply did its thing.

7. How energy widens India’s pension crisis

The earlier articles laid out a system already under strain: too few people covered, benefits too thin, savings raided too early, investment rules too tight to grow money fast. Energy inflation invents none of these problems. It just leans on every one of them.

The family that breaks into its provident fund years too soon — among the most corrosive habits for long-run adequacy — usually does it under exactly this kind of pressure. A run of dear fuel and dearer food is precisely what turns a sensible plan into a withdrawal slip. And the informal worker, who makes up most of India’s labour force and sits outside nearly every scheme, carries the thinnest buffer and spends the largest share of income on essentials. Most exposed to the shock, least shielded from it. The crisis and the energy bill meet hardest where the system already does the least.

The frozen ₹1,000 pension

If you want this in a single figure, look at the Employees’ Pension Scheme. Its minimum monthly pension was set at ₹1,000 in 2014 and has not moved since — more than a decade, through every cylinder hike and grocery rise in between, even after a parliamentary committee pointed out the obvious about how much living has cost over those years. Whatever thin dignity a thousand rupees a month offered in 2014, a decade of inflation has worn most of it away. It is the cleanest illustration going of a benefit that looked adequate the day it was written and was outdated within a year or two of the ink drying.

The annuity an NPS subscriber buys at retirement runs on the same logic. A conventional one pays a fixed rupee sum for life: a comfort at sixty, a slow squeeze by eighty, because every year inflation quietly trims what that fixed payment fetches. A fixed annuity is, when you strip it back, a wager that inflation will stay tame for the rest of your days — and the inflation-linked alternatives that would hedge it remain thin on the ground in the Indian market. The events of 2026 are a reminder of how that wager can go.

8. What a saver can actually do about it

None of this is a counsel of despair, mainly because the problem is so well understood. You can measure it, you can model it, you can build around it. What follows are considerations, not prescriptions — the right call depends on a life only you and a good adviser can see properly.

Plan in your own inflation, not the country’s. When you work out how big a corpus you need, run it on the rate your basket will actually face — weighted toward food, health and energy — not the headline. For a lot of retirees, 6 to 7% is nearer the truth than today’s 3.5%. The number it spits out is larger and less comfortable. It is also honest.

Give growth assets room over a long retirement. Thirty years is a long horizon, and a portfolio parked entirely in fixed income, earning a sliver of real return, can simply lose the race to inflation. A measured slice of growth — the equity options inside NPS, or other diversified vehicles — is one of the few things that has historically stayed ahead of rising prices over long stretches. It comes with volatility and suits some situations far better than others, which is exactly why it is a conversation to have with a professional rather than a rule to copy.

Treat energy as something you can partly hedge. Cutting your structural exposure to volatile fuel — efficient appliances, rooftop solar where the economics and the rooftop allow — turns a recurring, inflation-linked cost into a one-off outlay. For a retiree, shrinking the energy slice of the monthly budget works rather like handing the pension its own small inflation shield.

And insure against medical inflation on its own terms. With health costs compounding at double digits, a policy whose cover has stood still is, year by year, paying for a smaller and smaller share of any future bill. Reviewing that cover against medical inflation — not the headline — is one of the higher-return moves a near-retiree can make.

9. The fixes that are bigger than any one saver

There is only so far individual prudence stretches, and the energy problem keeps pointing back at the system. The recurring recommendations from people who study this are not exotic: a genuine minimum pension floor for the low-paid, coverage pushed out to informal and gig workers, firmer limits on early withdrawals, and more freedom for pension funds to hold the growth assets that can actually outrun inflation across decades. Each would make the whole structure steadier against precisely the kind of shock 2026 delivered.

There is also a specific case for building inflation protection into the products themselves. A system whose default payout is a fixed nominal annuity — or a floor frozen for ten years and counting — quietly hands every retiree a lifetime of inflation risk and calls it security. Wider access to inflation-linked retirement income, through indexed annuities or government-backed instruments, would meet the threat where it lives instead of leaving each household to fight it alone in their own kitchen.

10. The short version

- The rate in the headlines (~3.5% in early 2026) is not the rate a retiree pays; food, health and energy — most of an older household’s spending — have all run hotter.

- Medical inflation is the sharpest example: the CPI’s health component sits under 2%, while insurers peg real medical inflation near 12–14% a year.

- Energy stings twice — once through the gas, power and fuel bill, again through the energy cost buried inside almost everything else.

- The 2026 Strait of Hormuz disruption pushed a Delhi cylinder past ₹940 and fuel up ₹7.50 a litre — a live demonstration of how exposed Indian retirees are.

- Real return is the only return that counts: 8% nominal is barely 1% real against 7% lived inflation, and can go negative in a bad year.

The EPS minimum pension, stuck at ₹1,000 since 2014, shows how a fixed benefit rots; plan in real terms, give growth assets room, and insure against medical inflation specifically.

11. Questions readers ask

My corpus is large. Does inflation really matter?

Yes, because the corpus is a today-number and you will spend it in tomorrow-rupees. At 6% inflation, prices roughly double every twelve years, so a pile that looks ample at sixty can be worth half as much, in real terms, by your early seventies — without you touching a paisa more than planned.

Why does my cost of living climb faster than the official figure?

Because that figure averages a basket built for a typical household, and a retiree’s spending isn’t typical. Older people spend more on food, health and energy, which have been rising faster than the discretionary items pulling the average down.

I don’t drive. How does fuel inflation reach me?

Through everything else. Energy is an input into food, transport, medicines and services, so a fuel-price rise lands on your grocery and pharmacy bills even if you never buy a litre of petrol.

What can I do about it?

Plan around your own inflation rate, not the headline; keep a sensible allocation to growth assets over a long horizon; review health cover against medical inflation; cut structural energy exposure where you can; and know whether your annuity is fixed or inflation-linked. General considerations, not personal advice.

12. References

- Ministry of Statistics and Programme Implementation / Press Information Bureau — Consumer Price Index press releases, 2026 (headline CPI ~3.48% in April 2026; food inflation ~4.20%). https://www.mospi.gov.in

- Business Standard — “LPG prices hiked again by ₹29 per cylinder as costs surge globally,” 7 June 2026 (Delhi cylinder to ₹942; petrol/diesel +₹7.50/litre; ~54% of LPG via the Strait of Hormuz). https://www.business-standard.com

- International Institute for Sustainable Development — “Mapping India’s Energy Policy 2026,” April 2026 (Strait of Hormuz disruption; ₹60 LPG hike, 7 March 2026). https://www.iisd.org

- Press Information Bureau — “India’s Pension Landscape,” May 2026 (NPS AUM ~₹15.95 lakh crore as on 31 March 2026; EPS/EPFO structure). https://www.pib.gov.in

- Business Today — “EPFO, NPS, Atal Pension Yojana cover less than 25% of workers: Mercer report,” 18 October 2025 (Mercer–CFA Institute Global Pension Index 2025: India 45th of 47; ‘D’ grade; adequacy ‘E’ grade). https://www.businesstoday.in

- Business Today — “EPS pension hike: what changes if the minimum pension rises from ₹1,000 to ₹7,500?”, May 2026 (EPS minimum pension fixed at ₹1,000/month since 2014). https://www.businesstoday.in

- Milliman — “Measuring medical inflation in India,” 2026, with insurer trend surveys (Aon, WTW): medical inflation ~12–14% a year for 2025–26 versus a CPI health component near 1.6%. https://www.milliman.com

- Business Standard — “Retirement investing in 2025: key returns, hard lessons and the 2026 outlook,” December 2025 (EPF credited 8.25% for 2024–25). https://www.business-standard.com

Inflation, price and scheme figures reflect publicly reported data as of mid-2026 and are subject to revision. Infographic values are illustrative and rounded for clarity. This article is part of an educational series on retirement planning in India and is general information only — not financial, investment or tax advice. For guidance fitted to your own circumstances, consult a qualified financial adviser.

Amulya Charan writes on energy systems, infrastructure economics, and development policy at amulyacharan.com. This analysis draws on reporting from Business Standard, ThePrint, Business Today, and the Press Information Bureau, and on policy research from the Takshashila Institution and the Observer Research Foundation.