The Rupee Under Siege: What a ₹95 Dollar Means for Infrastructure Financing

Data snapshot: 23 June 2026 | Not financial, legal, tax, investment or hedging advice

Figure 1. Rupee-dollar picture at a glance: market levels, forecasts and infrastructure-relevant macro numbers.

1. Opening argument

On 21 May 2026, the rupee touched a fresh spot-market low near ₹96.96 to the dollar and closed around ₹96.82. By 22 June, it had recovered to roughly ₹94.63. That is not a full recovery so much as a more useful place to stress-test infrastructure projects. BMI, cited by PTI, expected the rupee to trade broadly around ₹95 per dollar by end-2026, but that is a forecast, not a certainty. [1][2][3]

For a household, a weaker rupee is usually an irritation: imported phones, overseas travel and fuel-linked costs get dearer. For infrastructure, it is more than a consumer-price story. The reason is simple: large parts of the build-out still depend on imported equipment, specialist inputs and foreign-currency financing.

A ₹95 dollar is not literally a tax, and it does not hit every project equally. A better way to frame it is as an implicit cost shock. It lands hardest on projects with open dollar procurement, imported kit, unhedged foreign-currency liabilities or fixed rupee revenues. Much of that impact is invisible in the headline capex number.

2. We have been here before, but the analogy needs care

India has seen currency stress expose infrastructure balance sheets before. During the 2013 taper-tantrum episode, a Harvard Business Publishing case study puts the rupee depreciation at about 13.7% from June to August 2013; some peak-to-trough measures are larger, but the safer point is not the exact percentage. [12]

The lesson is that foreign-currency debt can look cheap until the rupee moves after the project has already been bid, sanctioned or financially closed. Currency exposure was not the only cause of the later infrastructure bad-loan cycle. Land acquisition, fuel linkages, regulatory delays, aggressive bidding, stalled offtake arrangements and high leverage all mattered. But FX exposure added to the stress, and it did so at precisely the point when project cash flows were least flexible.

The 2026 episode is different in speed, policy response and macro context. Yet the project-finance trap is familiar: an exchange-rate assumption made at bid stage quietly reprices imported equipment, debt service and refinancing risk later.

3. How the rupee got near 95

Three forces pushed in the same direction through late 2025 and the first half of 2026.

First, monetary-policy divergence mattered. In December 2025, the RBI reduced the policy repo rate to 5.25% and maintained a neutral stance. That domestic easing was aimed at the Indian cycle, but a lower rate premium can reduce the cushion available to rupee assets when global investors reassess emerging-market exposure. [6]

Second, oil and geopolitics mattered. India imports most of its crude oil, so energy-price spikes tend to widen the import bill and put pressure on the external balance. RBI’s April 2026 Monetary Policy Report discussed West Asia conflict risks, elevated energy prices and imported inflation as part of the outlook. [4]

Third, the dollar did what the dollar often does in a risk-off moment. When global risk appetite weakens, capital tends to seek dollar safety, and emerging-market currencies absorb pressure even when the initial shock begins elsewhere.

The RBI has not simply watched the move. Market reports around the May low described public-sector banks selling dollars, a pattern traders often associate with central-bank intervention. But it is safer to say the RBI has tried to smooth volatility, not defend a fixed line at ₹95. RBI’s April 2026 forecast round used ₹94 per dollar as a baseline modelling assumption for FY2026-27; that is best read as an input to projections, not a promise about the exchange rate. [1][4][5]

Figure 2. Conceptual transmission channels from a weaker rupee into infrastructure costs.

4. The dollar hiding inside the capex budget

The headline capex story remains strong. Official Budget material put proposed public capital expenditure for FY2026-27 at about ₹12.2 lakh crore, roughly 9% higher than the previous year and far above the roughly ₹2 lakh crore public capex level in FY2014-15. [7]

The part the headline leaves out is import content. India is trying to deepen domestic capital-goods manufacturing, but modern infrastructure still needs equipment and inputs that are not always available locally at the required scale, precision or delivery timetable: tunnel-boring machines, turbines, signalling systems, solar components, specialist cranes, advanced safety systems and some high-grade materials. The same official Budget note said capital-goods imports rose 6.6% in Q1 FY26 and 9.2% in Q2 FY26. [7]

The arithmetic is straightforward. Take a ₹10,000 crore metro line with 35% imported equipment. At ₹85 to the dollar, the imported share is about ₹3,500 crore. At ₹95, identical dollar-priced equipment costs roughly ₹3,910 crore. The roughly ₹410 crore gap buys no extra tunnel, station or track. It is exchange-rate leakage.

As a rule of thumb, when imported content is 30% to 40% of a project, a 10% currency move can add roughly three to four percentage points to total capex before hedging, supplier price-locks or contractual pass-through. That is why the exchange rate belongs inside the project model, not in a macro appendix.

5. Where it bites hardest

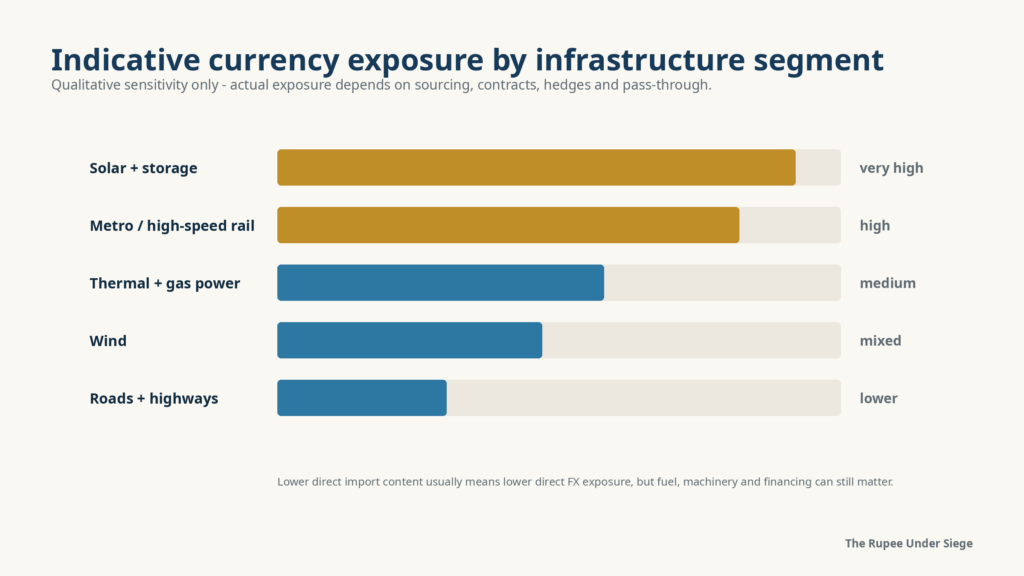

The pain is not spread evenly. Solar plus storage generally sits high on the exposure list because modules, cells and upstream components have historically carried import dependence, even as domestic capacity expands. Metro and high-speed rail projects can also be highly exposed through boring machines, rolling stock, power systems and signalling. Thermal and gas power face medium exposure through turbines, imported fuel linkages and specialty alloys. Wind is mixed: India has domestic wind-turbine manufacturing capacity, but some components, electronics and grid-integration equipment can still carry FX exposure. Plain roads and highways usually have lower direct FX exposure because earthwork, cement and aggregate are local, though imported machinery, bitumen, fuel and debt can still matter.

Figure 3. Qualitative sector sensitivity to currency moves. Actual project exposure depends on contracts, sourcing and hedging.

6. Then there is the debt

Equipment is only half the exposure. Financing is the other half. India’s external debt was reported at about $765.5 billion at end-December 2025. RBI data for March 2025 show that U.S.-dollar-denominated debt was the largest currency component of external debt, while loans were the largest instrument category. That distinction matters: dollar exposure is a currency question, not the same thing as saying every instrument is a dollar loan. [8][9]

For infrastructure borrowers, offshore credit can still be useful. It may provide longer tenor, a broader lender base or a lower visible coupon than domestic debt. The trap appears when the borrower earns largely in rupees but services debt linked to dollars.

Suppose a developer borrowed $500 million when the rupee was ₹83. The rupee value of principal was about ₹4,150 crore. At ₹95, the same dollar principal is about ₹4,750 crore. The project has not received more money, but its repayment burden has risen by about ₹600 crore. Interest, refinancing, covenant headroom and mark-to-market liquidity can move in the same direction.

This is not a case against foreign borrowing. It is a case against treating the offshore coupon as the whole cost of money. Once hedge costs, rollover risk and downside stress cases are included, some dollar borrowing remains sensible and some does not.

7. Solar is the clearest example, but not universal

Solar shows the currency mismatch clearly. Developers often bid or contract revenues in rupees, while a meaningful part of procurement can be linked directly or indirectly to dollar-priced components. If the rupee weakens between bid award and module or cell procurement, the cost line can move while the tariff line stays fixed.

But not every rupee of depreciation automatically passes through every solar project. Some projects hedge; some buy under rupee-denominated EPC contracts; some have change-in-law, pass-through or escalation provisions; some use domestic suppliers; and some procurement may already be locked in.

Regulatory language also needs precision. MNRE’s ALMM framework consists of List-I for modules and List-II for cells, with solar-cell applicability beginning in 2026 for specified project categories. Customs duties, cess, GST, domestic-content rules, ALMM eligibility and supplier constraints can all affect landed cost, but the effective impact depends on the exact product, tariff heading, exemption and procurement route. A single headline customs-duty number is therefore too crude. [13][14][15]

The safer conclusion is that a soft rupee can slow or reprice parts of the renewable build-out, especially where bids are aggressive and procurement is not yet fixed. It is one pressure among several, not the only villain.

8. The slower poison: inflation, rates and the cost of capital

A weaker rupee does not stop at invoices and loan schedules. It can seep into the whole cost of building through imported inflation. Crude, coking coal, some industrial metals, electronics, specialist machinery and freight all become more expensive in rupee terms when the currency falls, unless offset by global price declines or contractual protection.

That makes the RBI’s job harder. Imported input costs can keep inflation stickier, which narrows room for rate cuts. If domestic rates stay higher for longer, rupee borrowing costs rise even for projects with no explicit dollar debt. Foreign investors may also ask for more yield when currency risk is higher, lifting the floor under domestic infrastructure debt.

Uncertainty matters as much as the level. A steady ₹95 can be modelled. A ₹95 that might become ₹98 or ₹100 by the next procurement milestone pushes developers, lenders and suppliers to fatten contingencies or wait.

9. RBI’s 2026 ECB framework: more room offshore, fewer automatic guardrails

The February 2026 RBI amendment to the FEMA borrowing and lending framework materially liberalised external commercial borrowing. The borrowing limit is now framed as the higher of outstanding ECB up to $1 billion or total outstanding borrowing up to 300% of net worth; minimum average maturity is generally three years; and borrowing cost is to be in line with prevailing market conditions. Pre-existing ECBs with loan registration numbers issued before commencement of the amendment are generally governed by the pre-amendment framework unless specific amendment rules apply. [10][11]

The current framework gives borrowers and lenders more flexibility, but that flexibility should not be confused with safety. S&R Associates summarises the amended regulations as leaving foreign-exchange risk management to borrowers and lenders rather than imposing a single mandatory hedge ratio. In practice, lenders, boards and rating agencies may still require hedging; the point is that the all-in rupee risk must be assessed deal by deal. [10][11]

The catch remains real. Easier access to offshore debt can increase aggregate currency exposure if borrowers chase dollar funding without matching revenue, tenor and hedge policy. Hedges reduce FX risk, but they create other costs: forward premia, collateral or margin pressure, mark-to-market volatility, tenor mismatch and liquidity demands. The smart question is not simply “dollar or rupee debt?” It is “what is the all-in rupee cost after stress-testing and risk allocation?”

10. Running the scenarios

Since the exchange-rate assumption drives so much of the answer, the sensitivity should be shown plainly. The following illustrative case uses a ₹10,000 crore project, 35% imported equipment and a $300 million unhedged dollar loan drawn at ₹85. For a $300 million loan, every ₹1 depreciation adds about ₹30 crore to the rupee principal burden.

| Where the rupee lands | USD/INR | Extra equipment cost vs ₹85 | Extra rupee burden on $300m loan | Total extra cost |

| Base case | ₹92 | ~₹290 cr | ~₹210 cr | ~₹500 cr |

| Central forecast case | ₹95 | ~₹410 cr | ~₹300 cr | ~₹710 cr |

| Stress case | ₹98 | ~₹535 cr | ~₹390 cr | ~₹925 cr |

| Tail-risk case | ₹100 | ~₹620 cr | ~₹450 cr | ~₹1,070 cr |

Figure 4. Scenario chart for a representative project: imported equipment and dollar-debt burden move together.

The table is illustrative, not a project-finance model. It excludes hedges, supplier renegotiation, taxes, financing fees, inflation in local inputs and change-in-law effects. Its purpose is narrower: to show that currency moves can hit imported procurement and unhedged debt at the same time.

11. What this means for the people doing the building

For developers and EPC contractors, FX risk has moved from a treasury footnote to a bid-room issue. The danger often sits in the gap between quoting a rupee price and paying for imported equipment later. Useful mitigants include currency-escalation clauses, procurement hedges, supplier price-locks, staged buying, contingency budgets and credible domestic sourcing where quality and delivery schedules allow.

For lenders and infrastructure finance companies, the updated ECB framework offers more room offshore but demands more discipline. Stress cases at ₹95, ₹98 and ₹100 are not gloom; they are normal underwriting. The hedge ratio should reflect drawdown timing, debt-service dates, revenue currency, covenant headroom and liquidity capacity rather than a single headline percentage.

For policymakers, the long-run answer is deeper domestic capability in equipment and components. The Budget’s emphasis on capital goods and construction-equipment capacity points in the right direction. The transition period is harder: India needs the capex engine to keep running while the rupee is already soft and domestic supply chains are still scaling. Clear risk allocation in public procurement and concession contracts matters as much as headline spending.

For outside investors and analysts, the practical advice is simple: read infrastructure financials with the exchange rate beside them. The ₹12.2 lakh crore capex ambition says how much India wants to build. The FX sensitivity tells you how much of that ambition could be repriced before the asset is commissioned.

Figure 5. Practical FX-risk checklist for developers, lenders and policymakers.

11.The bottom line

A ₹95 dollar will not stop India building. Political will, public capex and infrastructure demand remain substantial. What it can do is make parts of the build-out costlier, more leveraged and more fragile than the official totals suggest.

The currency works through three channels at once: imported equipment, foreign-currency debt and the cost of capital. Each channel can be managed, but none should be ignored. The best-run projects will not be the ones that guess the next exchange rate perfectly. They will be the ones that know where a wrong guess hurts, who bears the cost, and how much protection is worth buying.

12. Method note and disclaimer

Figures are rounded and reflect data and public reporting available as of June 2026. Market prices, exchange rates and forecasts move daily. The worked examples are illustrative sensitivities, not project-finance valuations. This article is for information only and is not financial, legal, tax, investment or hedging advice.

References

[1] Times of India – Rupee hits 100/$ in 1-year forward, closes at 96.8 in spot trade

[2] Times of India – Rupee falls 30 paise to 94.63 against dollar amid Middle East uncertainty

[3] Outlook Business / PTI – Rupee to trade around ₹95/US dollar by end-2026: BMI

[4] Reserve Bank of India – Monetary Policy Report, April 2026

[5] Economic Times – RBI ups crude oil, exchange-rate baseline assumptions for FY27

[6] Reserve Bank of India – Monetary Policy Statement, 2025-26, December 3 to 5, 2025

[7] Press Information Bureau – Union Budget FY 2026-27: Strengthening Capital Goods Sector

[9] Reserve Bank of India – India’s External Debt as at the end of March 2025

[13] Ministry of New and Renewable Energy – Approved List of Models and Manufacturers (ALMM)

[14] Press Information Bureau – MNRE issues amendment to ALMM order for solar PV cells

————————————————————————————————————————————

Amulya Charan writes on energy systems, infrastructure economics, and development policy at amulyacharan.com.